Voda UK – Pump Up the Volume

The quarterly game of trying to analyse the mass of Voda Stats is upon us, please find enclosed my take: (*** see below for huge disclaimer and numerous assumptions)

Quarterly Net Adds were especially strong. Active Prepaid growth was around 357k to 8,012k which seems healthy, but Voda added more last Christmas (450k) and then seemed to spend calendar 2006H1 losing prepaid customers (1,018k), presumably as the base was cleaned up. However, the postpaid growth of 175k was the best for three years and followed up from 120k growth in the previous quarter. Voda UK is obviously gaining subscriber momentum in a saturated market. There is a question whether this growth is new customer to cellular, churners from other networks or even dual-triple SIM players, but it is a net positive.

However, this is hardly surprising given the tariff rebalancing of both prepaid and postpaid in the second half of the year. I calculate that the voice price per minute has dropped year-on-year by around 12.5% whereas the MOU has grown by around 13.9% and given the active base has dropped slightly y-o-y (0.9%), this leaves Voda slightly down on Voice Revenues. I believe that the growth in reported revenues (2.6%) y-o-y is from messaging and data revenues.

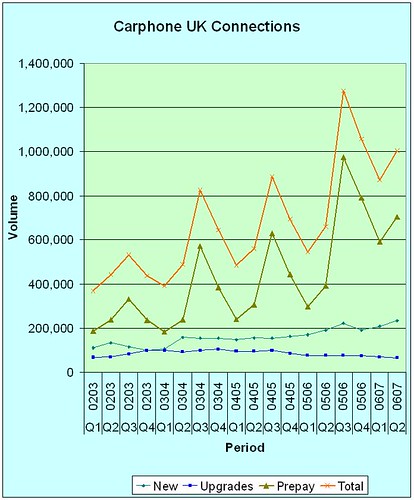

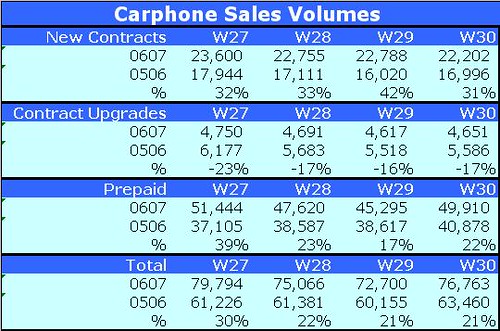

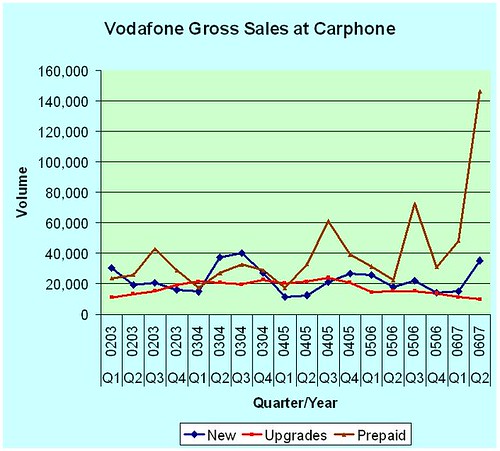

This price drop of tariffs together with the fact that the business segment is far more important to Voda than the consumer segment, obviously leads to confusion about whether the dropping of Carphone was worthwhile. Arun Sarin said on the call that net adds from both direct, indirect and Phones4U exceeded expectations. The justification for dropping Carphone was in terms of individual customer lifetime profitability and sales effort inconsistency so net adds are only a small part of the overall economics question. A slight insight in the overall UK SAC position would be extremely revealing if only Voda would provide the data.

The other part of the economics puzzle that Voda UK keeps extremely close to its chest is the percentage of on-net traffic. Obviously, the Voda family plan and some of the business tariffs are geared towards keeping as much as possible of the traffic on-net and incrementally the cost of carrying this traffic will be next to zero.

Churn although dropping is still humiliating high on both postpaid and prepaid bases even though the prepaid churn seems to been inflated by the base clean-up last year. Given the Voda share of the business and the typical miniscule churn, the churn on postpaid consumers must be horrific. This has to be the biggest challenge for Voda UK to overcome. In fact, it is an industry problem and I think that both length of contracts and distribution networks will feature as the key strategic concern in 2007 for all operators.

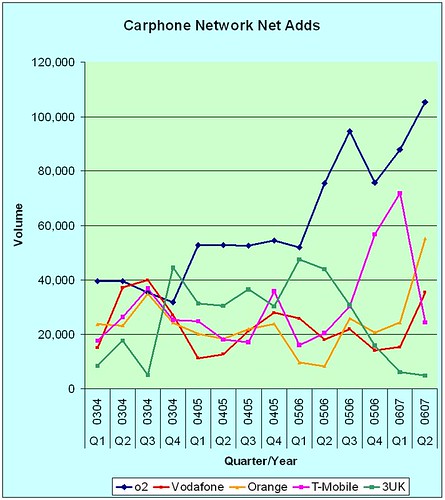

Overall, given these metrics and the momentum that o2 have generated during the year, I am almost certain that o2 have overtook Voda in q4 in terms of UK cellular revenue market share. However, I still think Voda will lead on profitability and cashflow. For the worlds leading mobile company to lose the #1 market position in its home market is embarrassing and gives hope to every Voda competitor throughout the world.

Given all this, I’m currently neutral on the Voda UK Fiscal Q3 performance. 2007 needs a dramatic improvement: it appeals to my sense of humour that it will probably take an Italian to reverse several years of lack of focus and poor decisions.

***Assumptions and Disclaimers:

#1: All inactive customers are prepaid: so of the claimed 16,939k customers with an inactive rate of 86.7% gives an active base of 14,686k customers.

#2: If the prepaid % is 60.6% then the contract % is 39.4% and these are all active: therefore active contracts customers are 6,674m and active prepaid are 8,012k

#3: ARPU needs to be adjusted for the inactives ratio to give ARPU of actives

#4: Average Quarterly Actives = (Current Quarter + Previous Quarter)/2

#5: % Revenue of Messaging and Data can be applied to Average Quarterly Active to give approx. Quarterly Revenue. Voice Revenue makes up the balance

#6: The differential between these service revenues and historic reported total revenues for the UK business is accounted for by equipment + other sales.

#7: These assumptions can be applied to all reported KPIs for the UK back to June 2004.

#8: All this is the opinion of Telebusillis, who has still not forgiven himself for not investing in Voda after any old fool should have spotted that Sir John Bond would have provided a short term impetus to the share price.

For those wishing to critique my assumptions or even enhance the humble model, email me and I will send by return a basic excel spreadsheet.

If anyone wants to complain about the size of the font for assumptions and disclaimers, I will only say people in glass houses shouldn't throw stones ;-)

Quarterly Net Adds were especially strong. Active Prepaid growth was around 357k to 8,012k which seems healthy, but Voda added more last Christmas (450k) and then seemed to spend calendar 2006H1 losing prepaid customers (1,018k), presumably as the base was cleaned up. However, the postpaid growth of 175k was the best for three years and followed up from 120k growth in the previous quarter. Voda UK is obviously gaining subscriber momentum in a saturated market. There is a question whether this growth is new customer to cellular, churners from other networks or even dual-triple SIM players, but it is a net positive.

However, this is hardly surprising given the tariff rebalancing of both prepaid and postpaid in the second half of the year. I calculate that the voice price per minute has dropped year-on-year by around 12.5% whereas the MOU has grown by around 13.9% and given the active base has dropped slightly y-o-y (0.9%), this leaves Voda slightly down on Voice Revenues. I believe that the growth in reported revenues (2.6%) y-o-y is from messaging and data revenues.

This price drop of tariffs together with the fact that the business segment is far more important to Voda than the consumer segment, obviously leads to confusion about whether the dropping of Carphone was worthwhile. Arun Sarin said on the call that net adds from both direct, indirect and Phones4U exceeded expectations. The justification for dropping Carphone was in terms of individual customer lifetime profitability and sales effort inconsistency so net adds are only a small part of the overall economics question. A slight insight in the overall UK SAC position would be extremely revealing if only Voda would provide the data.

The other part of the economics puzzle that Voda UK keeps extremely close to its chest is the percentage of on-net traffic. Obviously, the Voda family plan and some of the business tariffs are geared towards keeping as much as possible of the traffic on-net and incrementally the cost of carrying this traffic will be next to zero.

Churn although dropping is still humiliating high on both postpaid and prepaid bases even though the prepaid churn seems to been inflated by the base clean-up last year. Given the Voda share of the business and the typical miniscule churn, the churn on postpaid consumers must be horrific. This has to be the biggest challenge for Voda UK to overcome. In fact, it is an industry problem and I think that both length of contracts and distribution networks will feature as the key strategic concern in 2007 for all operators.

Overall, given these metrics and the momentum that o2 have generated during the year, I am almost certain that o2 have overtook Voda in q4 in terms of UK cellular revenue market share. However, I still think Voda will lead on profitability and cashflow. For the worlds leading mobile company to lose the #1 market position in its home market is embarrassing and gives hope to every Voda competitor throughout the world.

Given all this, I’m currently neutral on the Voda UK Fiscal Q3 performance. 2007 needs a dramatic improvement: it appeals to my sense of humour that it will probably take an Italian to reverse several years of lack of focus and poor decisions.

***Assumptions and Disclaimers:

#1: All inactive customers are prepaid: so of the claimed 16,939k customers with an inactive rate of 86.7% gives an active base of 14,686k customers.

#2: If the prepaid % is 60.6% then the contract % is 39.4% and these are all active: therefore active contracts customers are 6,674m and active prepaid are 8,012k

#3: ARPU needs to be adjusted for the inactives ratio to give ARPU of actives

#4: Average Quarterly Actives = (Current Quarter + Previous Quarter)/2

#5: % Revenue of Messaging and Data can be applied to Average Quarterly Active to give approx. Quarterly Revenue. Voice Revenue makes up the balance

#6: The differential between these service revenues and historic reported total revenues for the UK business is accounted for by equipment + other sales.

#7: These assumptions can be applied to all reported KPIs for the UK back to June 2004.

#8: All this is the opinion of Telebusillis, who has still not forgiven himself for not investing in Voda after any old fool should have spotted that Sir John Bond would have provided a short term impetus to the share price.

For those wishing to critique my assumptions or even enhance the humble model, email me and I will send by return a basic excel spreadsheet.

If anyone wants to complain about the size of the font for assumptions and disclaimers, I will only say people in glass houses shouldn't throw stones ;-)