3Q06: Telenor Blockbuster

Telenor released their 3Q results last Thursday to universal acclaim. However, something strikes me as slightly strange about the company and I’ve been mulling over this for a few days now.

This claiming of 100% ownership of the customers in partially owned subsidiaries is so last century and a warning bell to me that there is some sort of gaming going in attempting to prove growth.

Obviously and I stress this, I am not suggesting that Telenor is engaging in corrupt practices, but there is a risk to the underlying business model when a company operates in any corrupt country. I have basically dreamt up a metric (in co-operation with a currently anonymous third party) which gives an indication of this overall risk.

Basically, Telenor has a score which averages out to places like Bahrain and Jordan which to me is quite high. For a comparison, I ran the 3Q results of SingTel through the model and despite operating in places like Indonesia and The Phillipines, they came out significantly cleaner than Telenor.

I’m not sure if this risk is factored into the Telenor share price.

In 2005, Digi.com contributed NOK2,142m of EBITDA and NOK1,075m of Operating Profits which are just under 10% of the Telenor total. This is a significant amount to deconsolidate.

This might have seemed like a sensible strategy whilst the government was controlled by the owner of the major telecommunications competitor. However, he disposed of his stake in a "tax-free" manner to the investment arm of the government of Singapore. This seemed to have been the final straw for many members of the public and a military coup then ensued.

Telenor now faces a real uncertain future in Thailand and an investment of which they will probably will have to sell part of it. The question is how much money they will recover from the stake given that the buyer is probably local and they can't sell control for a premium. There is also the matter of deconsolidating the earnings and treating the whole venture as a financial investment in the future.

I'm not sure if the true extent of this political risk is factored into the value of Telenor.

The whole situation is extremely messy and I personally think could get even worse for Telenor, especially if Vimpelcom gets de-listed from the NASDAQ.

A drop in margins is not the end of the world, if absolute profits increase. I’d like to know how close to saturation these markets really are. Ukraine has 80% penetration and four mobile operators with two having really small market shares and well financed parent companies – the only action for them is to attack the leading player which is Kyivstar.

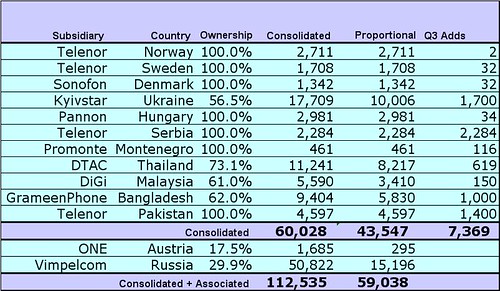

1. Subscriber Numbers

The first thing that struck me was the claim of having 105.2m subscribers. No matter how I slice and dice the numbers, I can’t reconcile to the Telenor claimed figure.This claiming of 100% ownership of the customers in partially owned subsidiaries is so last century and a warning bell to me that there is some sort of gaming going in attempting to prove growth.

2. Corruption Risk

Whenever anyone mentions Bangladesh to me, I always think that this is named in the annual Transparency International Corruption Perceptions Index as the most corrupt place on the planet.Obviously and I stress this, I am not suggesting that Telenor is engaging in corrupt practices, but there is a risk to the underlying business model when a company operates in any corrupt country. I have basically dreamt up a metric (in co-operation with a currently anonymous third party) which gives an indication of this overall risk.

Basically, Telenor has a score which averages out to places like Bahrain and Jordan which to me is quite high. For a comparison, I ran the 3Q results of SingTel through the model and despite operating in places like Indonesia and The Phillipines, they came out significantly cleaner than Telenor.

I’m not sure if this risk is factored into the Telenor share price.

3. Political Risk

i. Malaysia

Telenor owns 61% in its' Malaysian subsidiary digi.com. Unfortunately, the law only allows foreign companies to hold 49%. Therefore, Telenor has to sell 12% of its' holdings and treat the investment as an associate. Telenor has known about this since increasing its' stake from 32.9% to 61% (increase of 28.1%) via market purchases for NOK3.2bn (US$490m) in Sept 2001. digi.com is floated and current market capitalisation is US$2.44bn.In 2005, Digi.com contributed NOK2,142m of EBITDA and NOK1,075m of Operating Profits which are just under 10% of the Telenor total. This is a significant amount to deconsolidate.

ii. Thailand

Thailand also has a law restricting foreign ownership to 49%. However in 2005, Telenor performed a series of complex transaction with holding companies to increase its' effective ownership to 70.6%. It effectively paid NOK1.2bn for an additional 18.2% of the mobile company. This puts a valuation of the company at around US$1bn. Telenor consolidated the Thai asset in its' accounts in 2005 with a book value of NOK 6170m (approx. US$943m)This might have seemed like a sensible strategy whilst the government was controlled by the owner of the major telecommunications competitor. However, he disposed of his stake in a "tax-free" manner to the investment arm of the government of Singapore. This seemed to have been the final straw for many members of the public and a military coup then ensued.

Telenor now faces a real uncertain future in Thailand and an investment of which they will probably will have to sell part of it. The question is how much money they will recover from the stake given that the buyer is probably local and they can't sell control for a premium. There is also the matter of deconsolidating the earnings and treating the whole venture as a financial investment in the future.

iii. Bangladesh

An election is due next year which could change the rules of the game significantly. Also the current government have cut the interconnect rates by 20%.iv. Pakistan

Enough said without going into the problems Telenor faced after a Danish joke went down badly.I'm not sure if the true extent of this political risk is factored into the value of Telenor.

4. Partner Risk

The partner of Telenor in the important Russian and vitally important Ukrainian venture is the legendary Alfa Bank (via Altimo). To say that Telenor and Alfa do not see eye to eye would be the understatement of the century. Vimpelcom have already launched a subsidiary in the Ukraine to compete with Kyivstar. Just today Vimplecom have announced they will bid for a licence in Montenegro, which is where Telenor already operate.The whole situation is extremely messy and I personally think could get even worse for Telenor, especially if Vimpelcom gets de-listed from the NASDAQ.

5. Profit Risk

I am completely on my own on this one, but I feel that the high margins that Telenor make in the third world are not sustainable. In Bangladesh, Telenor makes Operating Profit margins of 42% and EBITDA margins of 57% - these are extremely high. It is not going to take a genius in the Bangladeshi government or even worse some NGO peacenik to claim that these are excessive returns for one of the poorest places on the planet. In the Ukraine the situation is even worse, Operating Profit Margins of 47% and EBITDA margins of 60%. In Serbia, Operating Profit Margins of 48% and EBITDA of 59% - I can easily see a third entrant (Vimpelcom) finding these margins attractive.A drop in margins is not the end of the world, if absolute profits increase. I’d like to know how close to saturation these markets really are. Ukraine has 80% penetration and four mobile operators with two having really small market shares and well financed parent companies – the only action for them is to attack the leading player which is Kyivstar.

<< Home