3Q06: US Cellular Majors

The US Major Cellular companies have finished reporting for the 3Q and there are three main stories: Verizon’s relentless pursuit of Cingular in terms of being the leader for subscribers and service revenues; Cingular improvement in margins; and Sprint’s decline.

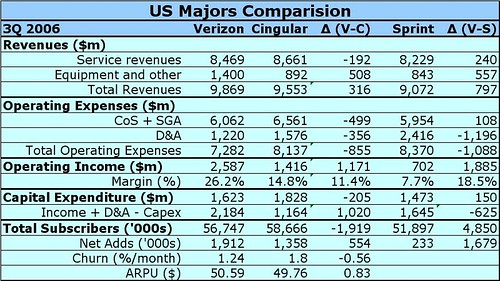

Verizon Wireless are already stating that they are the leader in Retail Subscribers (i.e. excluding Wholesale) and Total Revenue (i.e. including handset sales). Personally, I think these statements of being the leader on these counts are a little premature – the metrics that matter to me are Service Revenue and Total Subscribers. The gap in total subscribers is narrowing down from 3m a year ago to 1.9m today; similarly the gap in Service revenues is also narrowing down from US$451m a year ago to US$192m today. If the market continues on its’ current path, I expect Verizon Wireless to be the undisputed market leader on all metrics by this time next year. What is without doubt is that Verizon Wireless is gaining market share by any metric. The Christmas quarter may see a slight fillip to the relative position of Cingular, but this will reflect the higher share of pre-paid customers, whether retail or wholesale, on their base rather than any underlying market gains.

The metric that is king for me is operating margin and there is no doubt that Cingular is catching up Verizon on this one. Cingular’s Operating Margin has shot up from 7.5% one year ago to 14.8% today. This is truly a fantastic achievement and the COO of Cingular, Ralph de la Vega, who has been driving the integration of the old AT&T and Cingular deserves every single bit of credit that he is receiving. The integration is not complete and Cingular still has to turn off its’ analogue network and transition the TDMA customers (of which there are 3.6m); these events are due in early 2008 and it will be extremely interesting to compare margins at this time. Cingular are absolutely adamant that they can catch Verizon and although I believe the bar may be set too high, I am less of a disbeliever today than I was back in early 2004 at the time of the merger. When Seidenberg was asked the question in the Q&A session today, he implied that by the time Cingular catches Verizon, Verizon will have moved on. To prove his point Verizon has moved on from 21.8% operating margin one year ago to 26.2% today.

To me the key question, which Seidenberg ducked, is when growth will slow down. Annual Service Revenue growth for Verizon is 16.5% and for Cingular is 12.2%. It is relatively easy improve margins when revenue growth is so strong. The European market shows that margins are quick to decline when growth in the top line stops. Alltel mentioned in their 3Q call that in the major US metropolitan markets, it is extremely difficult to compete with Verizon and Cingular. We are seeing big markets share gains by both and realistically I can see both Sprint and T-Mobile (from a lot lower base) being weak for another couple of years and then perhaps they will joined by the cable companies. After that, if any growth is left it will be heavily fought for and stagnation could trigger a price war. The keys will be how Cingular and Verizon decide to expand into secondary markets, either organically or via acquisition and whether either decide to focus into specific niches eg prepaid, which will send shivers down the MVNO spines.

Finally, it is really sad to see the decline of Sprint after the acquisition of Nextel: I think the appalling results are just a reflection of a confusing strategy. Cingular after their merger with AT&T bit the bullet and went all out to move everyone onto GSM technology, committing to the GSM route to advanced services. Sprint in their heart of hearts must know that iDen is a dying network technology, but they are apparently making no effort to transition the customers to CDMA. It appears that Verizon is stepping into the void and doing the job for them. The whole Nextel merger appears to me to be an ill-thought out knee jerk reaction to the size of Cingular and Verizon.

Convergence has been in the news for the last couple of years and obviously Cingular (SBC & BellSouth) and Verizon have large fixed-line base to sell convergent services into. Ever since I can remember, Sprint has blown tones of cash trying to develop a local loop path. The latest attempt of getting into bed with the Cable Companies seems fatally flawed to me. The recent AWS Auction 66 has only reinforced my initial beliefs.

Why Sprint would risk everything in the pursuit of immediate bulk and a mythical convergent offering is beyond me. I suspect that Sprint will struggle along for the next few years until the cable companies are ready to digest it.

Verizon Wireless are already stating that they are the leader in Retail Subscribers (i.e. excluding Wholesale) and Total Revenue (i.e. including handset sales). Personally, I think these statements of being the leader on these counts are a little premature – the metrics that matter to me are Service Revenue and Total Subscribers. The gap in total subscribers is narrowing down from 3m a year ago to 1.9m today; similarly the gap in Service revenues is also narrowing down from US$451m a year ago to US$192m today. If the market continues on its’ current path, I expect Verizon Wireless to be the undisputed market leader on all metrics by this time next year. What is without doubt is that Verizon Wireless is gaining market share by any metric. The Christmas quarter may see a slight fillip to the relative position of Cingular, but this will reflect the higher share of pre-paid customers, whether retail or wholesale, on their base rather than any underlying market gains.

The metric that is king for me is operating margin and there is no doubt that Cingular is catching up Verizon on this one. Cingular’s Operating Margin has shot up from 7.5% one year ago to 14.8% today. This is truly a fantastic achievement and the COO of Cingular, Ralph de la Vega, who has been driving the integration of the old AT&T and Cingular deserves every single bit of credit that he is receiving. The integration is not complete and Cingular still has to turn off its’ analogue network and transition the TDMA customers (of which there are 3.6m); these events are due in early 2008 and it will be extremely interesting to compare margins at this time. Cingular are absolutely adamant that they can catch Verizon and although I believe the bar may be set too high, I am less of a disbeliever today than I was back in early 2004 at the time of the merger. When Seidenberg was asked the question in the Q&A session today, he implied that by the time Cingular catches Verizon, Verizon will have moved on. To prove his point Verizon has moved on from 21.8% operating margin one year ago to 26.2% today.

To me the key question, which Seidenberg ducked, is when growth will slow down. Annual Service Revenue growth for Verizon is 16.5% and for Cingular is 12.2%. It is relatively easy improve margins when revenue growth is so strong. The European market shows that margins are quick to decline when growth in the top line stops. Alltel mentioned in their 3Q call that in the major US metropolitan markets, it is extremely difficult to compete with Verizon and Cingular. We are seeing big markets share gains by both and realistically I can see both Sprint and T-Mobile (from a lot lower base) being weak for another couple of years and then perhaps they will joined by the cable companies. After that, if any growth is left it will be heavily fought for and stagnation could trigger a price war. The keys will be how Cingular and Verizon decide to expand into secondary markets, either organically or via acquisition and whether either decide to focus into specific niches eg prepaid, which will send shivers down the MVNO spines.

Finally, it is really sad to see the decline of Sprint after the acquisition of Nextel: I think the appalling results are just a reflection of a confusing strategy. Cingular after their merger with AT&T bit the bullet and went all out to move everyone onto GSM technology, committing to the GSM route to advanced services. Sprint in their heart of hearts must know that iDen is a dying network technology, but they are apparently making no effort to transition the customers to CDMA. It appears that Verizon is stepping into the void and doing the job for them. The whole Nextel merger appears to me to be an ill-thought out knee jerk reaction to the size of Cingular and Verizon.

Convergence has been in the news for the last couple of years and obviously Cingular (SBC & BellSouth) and Verizon have large fixed-line base to sell convergent services into. Ever since I can remember, Sprint has blown tones of cash trying to develop a local loop path. The latest attempt of getting into bed with the Cable Companies seems fatally flawed to me. The recent AWS Auction 66 has only reinforced my initial beliefs.

Why Sprint would risk everything in the pursuit of immediate bulk and a mythical convergent offering is beyond me. I suspect that Sprint will struggle along for the next few years until the cable companies are ready to digest it.

Finishing off, Verizon had winning bids of US$2.8bn in Auction 66 compared to approximately US$2.2bn in quarterly operating cashflow. Note, I approximate cashflow as Operating Income adding in the non-cash depreciation and amortization and subtracting the Capital Expenditure. Obviously, this is missing the change in working capital, but is useful as a ball-park figure. My point is that Verizon got a lot of spectrum for not a lot of cashflow, especially when you compare it to some of the risks taken by the smaller players.

<< Home