The House that Subsidy Built

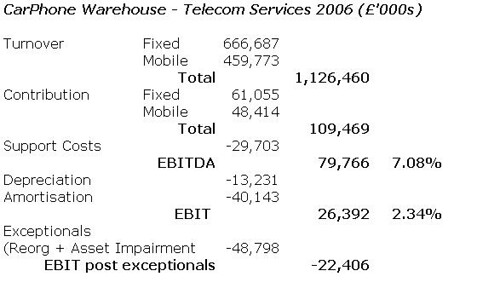

So, when the presentation of the results is slightly changed it reveals all is not well at Carphone Warehouses Services division which is basically an attempt to diversify away from operator subsidies.

In trying to discover the real return, it is probably worthwhile examining how much Carphone Warehouse has spent on this division.

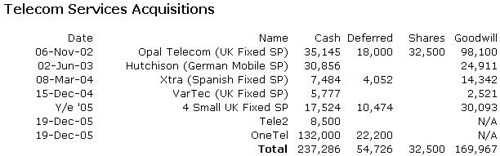

Obviously, CPW has spent heavily investing in buying services businesses which currently is not providing a return. Please do not ignore the deferred consideration in the mental arithmetic of costs, because according to the accounts the Opal Telecom deferment of £18m was paid in full. The details of the goodwill calculation for Tele2 and One.tel will only be available later in the month when the published accounts are made available. However, it is worth noting that as at 1st April 2006, the CPW balance sheet contained £568m of Goodwill and £159m of “Other Intangible Assets”, this includes capitalized SAC costs. Although, the whole of these line items are not fully attributable to Telecom Services, I would guess a vast proportion is as the majority of historical acquisitions are in the services arena. All I can really say is that profits better start flowing soon from the fixed division or else exception write-offs will become the norm rather than exceptional in nature. The Vodafone CFO can potentially provide advice on the pain of annual impairment tests.

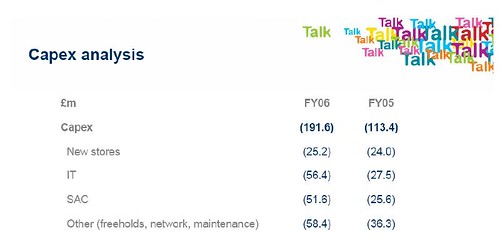

Of course, acquisitions do not provide the whole picture but as BT will testify the capital costs of continually upgrading the network is quite onerous. Again there are only partial clues to how much CPW is spending here.

However, the conclusion is clear Capex is exploding – this is a typical feature of a telco and does not fit into the typical retailer profile. It is also interesting that both the complexity of business is increasing (visible by an increase in IT development costs) and that Carphone Warehouse is now also joining the SAC game as opposed to just being a recipient of SACs via the subsidies that operator provide to the retail business.

All of this is before the LLU business was launched and Dunstone delivered the PR stunt of the year where the decimation of earnings for FY07 was presented as a great success. For sure, every customer is delirious, I’ve even bought the service myself, but the conundrum for the shareholder is why is Dunstone doing this?

I must admit to following the fortunes of CPW for most of this decade, this is primarily because Dunstone built a huge business out of nothing in an industry full of sharks and has emerged with a fantastic reputation: in other words I think he has done a fantastic job and deservedly built a fortune at the same time.

The big wild-card for me was the purchase of Opal and launch into the consumer altnet market with TalkTalk. I watched with amazement as he doubled the bet with the purchase of one.tel/tele2 and then doubled the bet again with the launch of “Free Broadband Forever”.

My initial impression was that he was desperate to diversify away from the dependency of his group on operator subsidies. After all, if every mobile operator is expanding their owned distribution network, proclaiming that subsidies have to be reduced and the market is saturated with everyone focusing on costs, even a laid back character like me would start to feel a little paranoid. However, to me it is becoming increasing apparent that a decent return in the fixed arena is going to become difficult to achieve.

I’m now completely of the belief that Dunstone is playing the asset value game and not at all worried about the short-term profit and loss. One thing that I’m certain about is that he will not leave it up to the Private Equity Companies to realize the value as the current Caudwell plan.

For instance, how much do you think that o2/telefonica, t-mobile/deutsche telecom, Vodafone will pay to become overnight the leading UK alternative provider??

I was extremely shocked in the conference call by the flippant comment that Charles Dunstone dismissed the current Orange/Wanadoo offer. After all it hardly the biggest secret on the planet that the key to getting the best mobile deal is walking down to local Carphone Warehouse, trying out the handsets, picking the best tariff and then ringing your current provider asking for a PAC code and then watch them beat the CPW offer. It is almost as if Charles is juggling with several bits of live Semtex, he could escape safely, but equally it could endup in tears.

If Dunstone makes the perfect final move and extracts a huge premium from one of the mobile operators for a low margin declining business covering all his past follies, I will doff my cap…

<< Home