AWS-1 Auction – Day 3 Summary

Another day, another US$952,823,305 into the US government coffers.

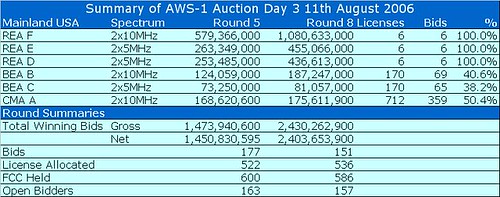

The price of a mainland US licence in the “F” band has crossed the threshold of US$1bn. The price differential between the equivalent “A” band and “B” band is growing huge at 6.15x and 5.77x.

It is difficult to analyse bidder intentions during the progress of an auction because some of the moves may just be bluffs. It is akin to analyzing a poker game without the privilege of seeing the hands that the players hold. Mind you, the Monday Morning Quarterbacking that goes on post-auctions is also fraught with difficulties as people re-invent history and intentions to prove that they are brilliant after all. It is almost as if everyone takes a cognitive dissonance pill on the night of auction exit and wake in the morning with a whole new view on the world.

I think Verizon Wireless and Atlantic Wireless are exhibiting strange behaviour. First of all, Verizon Wireless is bidding on every supa-region of mainland USA in the “F” band except the North East. Atlantic Wireless is similarly only bidding in the “F” band and only on the North East region. Each is just bidding by the minimum increment each round. This is probably just a weird statistical freak because collusion is not permitted. Atlantic Wireless is a new company which qualifies for the 25% discount for new entrants and reputedly is financed by the same people behind Aloha partners who already hold some spectrum in the WiMax bands.

In 2000, one of the Verizon Wireless partnership, Vodafone, employed a similar tactic in the UK 3G auctions. Everyone knew before the start of the auction that Vodafone was by far and away both the strongest financially and had the biggest market share in the UK. Vodafone just sat on the license with the highest amount of available frequency (30MHz) and let the rest of the incumbents fight for the remaining 20MHz licenses on offer. Vodafone never budged from the 30Mhz license during the auction process. If it wasn’t for BT who was determined to force Vodafone to pay a realistic price for the extra spectrum, Vodafone would bought the extra frequency at a big theoretical discount. In the end Vodafone got the license at between 1.47x and 1.49x the price of the smaller licenses. Only time will tell whether Vodafone bought too much frequency but the Monday Morning Quarterbacks who egged all the bidders on during the auction now claim all the bidders were idiots who vastly overpaid.

There was also a rather grand gesture by T-Mobile this evening in Round 8 who bid more than the minimum (a 20% increase) on every “F” license that it was permitted to bid on and therefore won every bid. Personally, I think the tactic is so that T-Mobile will be featured in all the weekend press as the auction leader. Also, it meant the total spend of T-Mobile was just over a headline grabbing US$1bn. T-Mobile isn’t bluffing me – it is desperate for the extra spectrum and will pay whatever is necessary. The T-Mobile mothership, Deutsche Telekom, announced on Thursday that USA cash flow was around US$1bn for the first six months of the year. All of this is at risk if T-Mobile doesn’t buy enough spectrum to launch next generation services in the key US markets. Therefore, T-Mobile will continue bidding until enough people pull out and leaves it with the necessary spectrum. Then the T-Mobile and Deutsche Telekom executives will breathe a huge sigh of relief and hope that too much damage hasn’t been done to the shareprice of the mothership.

Rather than the Peacock-esque behaviour of the mega-bidders, the more interesting fights at this early stage are breaking out in the rural areas. I’ll try to look at some of smaller players over the weekend.

The price of a mainland US licence in the “F” band has crossed the threshold of US$1bn. The price differential between the equivalent “A” band and “B” band is growing huge at 6.15x and 5.77x.

It is difficult to analyse bidder intentions during the progress of an auction because some of the moves may just be bluffs. It is akin to analyzing a poker game without the privilege of seeing the hands that the players hold. Mind you, the Monday Morning Quarterbacking that goes on post-auctions is also fraught with difficulties as people re-invent history and intentions to prove that they are brilliant after all. It is almost as if everyone takes a cognitive dissonance pill on the night of auction exit and wake in the morning with a whole new view on the world.

I think Verizon Wireless and Atlantic Wireless are exhibiting strange behaviour. First of all, Verizon Wireless is bidding on every supa-region of mainland USA in the “F” band except the North East. Atlantic Wireless is similarly only bidding in the “F” band and only on the North East region. Each is just bidding by the minimum increment each round. This is probably just a weird statistical freak because collusion is not permitted. Atlantic Wireless is a new company which qualifies for the 25% discount for new entrants and reputedly is financed by the same people behind Aloha partners who already hold some spectrum in the WiMax bands.

In 2000, one of the Verizon Wireless partnership, Vodafone, employed a similar tactic in the UK 3G auctions. Everyone knew before the start of the auction that Vodafone was by far and away both the strongest financially and had the biggest market share in the UK. Vodafone just sat on the license with the highest amount of available frequency (30MHz) and let the rest of the incumbents fight for the remaining 20MHz licenses on offer. Vodafone never budged from the 30Mhz license during the auction process. If it wasn’t for BT who was determined to force Vodafone to pay a realistic price for the extra spectrum, Vodafone would bought the extra frequency at a big theoretical discount. In the end Vodafone got the license at between 1.47x and 1.49x the price of the smaller licenses. Only time will tell whether Vodafone bought too much frequency but the Monday Morning Quarterbacks who egged all the bidders on during the auction now claim all the bidders were idiots who vastly overpaid.

There was also a rather grand gesture by T-Mobile this evening in Round 8 who bid more than the minimum (a 20% increase) on every “F” license that it was permitted to bid on and therefore won every bid. Personally, I think the tactic is so that T-Mobile will be featured in all the weekend press as the auction leader. Also, it meant the total spend of T-Mobile was just over a headline grabbing US$1bn. T-Mobile isn’t bluffing me – it is desperate for the extra spectrum and will pay whatever is necessary. The T-Mobile mothership, Deutsche Telekom, announced on Thursday that USA cash flow was around US$1bn for the first six months of the year. All of this is at risk if T-Mobile doesn’t buy enough spectrum to launch next generation services in the key US markets. Therefore, T-Mobile will continue bidding until enough people pull out and leaves it with the necessary spectrum. Then the T-Mobile and Deutsche Telekom executives will breathe a huge sigh of relief and hope that too much damage hasn’t been done to the shareprice of the mothership.

Rather than the Peacock-esque behaviour of the mega-bidders, the more interesting fights at this early stage are breaking out in the rural areas. I’ll try to look at some of smaller players over the weekend.

<< Home