AWS-1 Auction 66

Two days to go and I’m getting pretty psyched – all the ingredients are prepared and thrown into the mixing bowl - I'm ready for a fiercely fought and therefore expensive auction.

This is not the same frequency band as the UMTS spectrum licensed in Western Europe and Japan. So dual-mode phones will be needed for UMTS roaming services to work cross continents. Personally, over time this is not a big problem as quad-band GSM phones have overcome this problem in the past. I’m sure that the proportion of total Bill of Material cost for this extra functionality will be minimal in the overall scheme of a multi-baseband 3G phone.

Anyway, the US internal market is so big who really cares about roaming?

I’m sure that some companies will be considering deploying non-standard 3G technologies (ie apart from EV-DO and UMTS) – hopefully, we may see some companies trying to deploy OFDM based technologies.

The argument goes that as AT&T Wireless and Nextel have disappeared as independent companies from the market then there will less demand for the spectrum. I really, really doubt it. Spectrum is the oxygen that wireless companies breathe: the more they have the more things they can do. Any new entrant wanting to offer a wireless service using exclusive spectrum has to compete in these auctions: otherwise they have to rely on unreliable unlicensed shared spectrum.

More importantly, after all the expense of consolidation, I’m 100% positive that the huge wireless companies will pay huge premiums (in the form of license fees) to keep their club as small as possible: Verizon Wireless, Cingular and T-Mobile will fight to keep anyone else from owning a nationwide license and more importantly to keep potential customers out of the key Top 10 markets. Sprint is a more complicated matter and more of that later.

All other previous spectrum auctions have been based upon a patchwork of licensees across the USA covering as many as 714 areas or at a minimum 176 licenses. Although this policy has allowed the emergence of small rural providers, it has meant that not one single wireless provider covers 100% of mainland USA.

This auction is different: mainland USA can be covered by only winning 6 regional licenses! There are 2 blocks of 10MHz and 1 block of 20MHz – expect these blocks to be fiercely contested.

It should not be forgotten that these licenses are as valuable for Verizon Wireless and Cingular as they are for a new entrant. For instance if Verizon got 10Mhz in all these 6 blocks – it could:

• slowly but surely build out the network in areas where they currently have high roaming charges with 3rd parties;

• as the Top 100 markets become saturated move into new smaller markets where before Verizon has had no presence leveraging its’ economies of scale and pushing the current small rural players into submission – a sort of WalMart Wireless strategy.

In other words, it would have the capability of both reducing ongoing costs and improving market coverage and therefore revenue and profitability growth. A similar story applies to Cingular.

The same arguments apply for T-Mobile however because they are currently spectrum challenged, they need to buy as much spectrum as possible. If T-Mobile don't buy enough spectrum in enough markets, they will be forced to be a pure voice and sms seller. Verizon and Cingular will know the T-Mobile weak spots and poor coverage: they will fight to keep the weak spots weak and thereby keep T-Mobile weak.

Sprint Nextel is someone who I believe isn’t really interested in this auction, mainly because of bigger internal challenges. I think the process is being driven by TimeWarner and Comcast. I expect to see SpectrumCo (the name of their JV) to bid strongly in the markets where the cables companies have licenses, so if the holy grail of triple and quad plays actually work they have spectrum to fight AT&T/Cingular and Verizon without all of the proceeds going to Sprint Nextel.

The most intriguing bidder is DirectTV, EchoStar and LibertyOne aka Wireless DBS. As we see from exploits of Murdoch in the UK via BSkyB – satellite is going interactive and I think Auction 66 is one of the few possibilities of having a return path in the USA. I suspect if successful, the whole US Satellite industry will be restructured and the inclusion of John Malone’s LibertyOne signals to me that they are prepared to bid more than DirectTV and EchoStar could afford together. The placing of a near US$1bn deposit signals to everyone that this partnership is serious and going to bid strong.

That is enough players to ensure that the Regional mega-licenses are sold for a lot of money: Verizon, Cingular, T-Mobile and Wireless DBS cannot carve up 4 nationwide licenses when there are only 3 on offer.

In addition in huge auctions there are always silent players sat on sidelines waiting for an opportunity. An example of this was the huge bidding in the UK 3G auction by TIW of Canada which remained a mystery until it was revealed that Hutchison of Hong Kong were behind them. There will be plenty of wireless arbitragers sat on the sidelines, watching and willing to buy a seat on the table in the middle of the poker (oops sorry auction) game if necessary.

One of the great things about the US auctions is the amount of players who are willing to risk a lot of capital, including the major players named above there are 168 bidders qualified: 9 have placed deposits over US$100m; 8 have placed deposits between US$80m and US$10m; 30 have placed deposits between US$10m and US$1m; and 121 less than US$1m.

For instance, Leap Wireless aka Cricket have placed a deposit of US$255m on the auction. Leap Wireless specialise in building low cost networks in smaller cities - that is a big deposit for purely small cities. Perhaps they have a mystery backer for moving into the bigger cities?

In fact, there are professional players in the US Auctions who are basically just shopping for bargains to be later re-sold. The existence of these players is enough to ensure that prices are kept high. There is more than enough bidders to keep the bidding even on the smaller licenses fair and square. In we add into the equation that the majors will want to keep minor players out of the Top 100 markets means bidding will be fierce even on the blocks A-C.

I’ve heard more than a couple of people say 3G services are a big disappointment and therefore no-one will bid a lot for the licenses.

The truth is that Verizon have just reported that their quarterly non-SMS data has climbed above US$500m per quarter and that by my calculation Free Cash Flow was about US2bn in the first six months of the year. Cingular have also just reported record profits. That is a lot of profit both to go after and more importantly to protect.

Total Rubbish – for evidence, look at the recent auction of some African assets.

The US government estimates that they will receive around US$15bn from the auction – that is a real low figure and if this is all they receive the Big Cellular companies will be extremely happy. After all, it is just 4 years of Free Cash Flow for Verizon: in other words Verizon could buy every single license on offer and without any additional sales will be in the money after 4 years of a 15 year license.

The reason that auctions realise a lot of money is from the auction design – a lot of people with a lot of money and a lot to lose need to compete for a scarce resource.

That is the environment with Auction 66 and I’ll be extremely surprised if in a couple of week’s time everyone (apart from me) isn’t amazed at the prices being discussed.

US$30bn is the minimum I’m expecting…

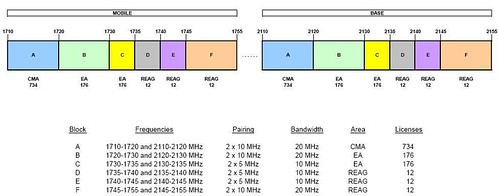

Frequency Band

This is not the same frequency band as the UMTS spectrum licensed in Western Europe and Japan. So dual-mode phones will be needed for UMTS roaming services to work cross continents. Personally, over time this is not a big problem as quad-band GSM phones have overcome this problem in the past. I’m sure that the proportion of total Bill of Material cost for this extra functionality will be minimal in the overall scheme of a multi-baseband 3G phone.

Anyway, the US internal market is so big who really cares about roaming?

I’m sure that some companies will be considering deploying non-standard 3G technologies (ie apart from EV-DO and UMTS) – hopefully, we may see some companies trying to deploy OFDM based technologies.

Market Consolidation

The argument goes that as AT&T Wireless and Nextel have disappeared as independent companies from the market then there will less demand for the spectrum. I really, really doubt it. Spectrum is the oxygen that wireless companies breathe: the more they have the more things they can do. Any new entrant wanting to offer a wireless service using exclusive spectrum has to compete in these auctions: otherwise they have to rely on unreliable unlicensed shared spectrum.

More importantly, after all the expense of consolidation, I’m 100% positive that the huge wireless companies will pay huge premiums (in the form of license fees) to keep their club as small as possible: Verizon Wireless, Cingular and T-Mobile will fight to keep anyone else from owning a nationwide license and more importantly to keep potential customers out of the key Top 10 markets. Sprint is a more complicated matter and more of that later.

Potential “Once in a Life” Opportunity

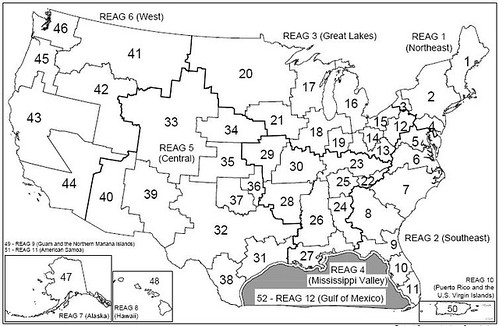

All other previous spectrum auctions have been based upon a patchwork of licensees across the USA covering as many as 714 areas or at a minimum 176 licenses. Although this policy has allowed the emergence of small rural providers, it has meant that not one single wireless provider covers 100% of mainland USA.

This auction is different: mainland USA can be covered by only winning 6 regional licenses! There are 2 blocks of 10MHz and 1 block of 20MHz – expect these blocks to be fiercely contested.

It should not be forgotten that these licenses are as valuable for Verizon Wireless and Cingular as they are for a new entrant. For instance if Verizon got 10Mhz in all these 6 blocks – it could:

• slowly but surely build out the network in areas where they currently have high roaming charges with 3rd parties;

• as the Top 100 markets become saturated move into new smaller markets where before Verizon has had no presence leveraging its’ economies of scale and pushing the current small rural players into submission – a sort of WalMart Wireless strategy.

In other words, it would have the capability of both reducing ongoing costs and improving market coverage and therefore revenue and profitability growth. A similar story applies to Cingular.

The same arguments apply for T-Mobile however because they are currently spectrum challenged, they need to buy as much spectrum as possible. If T-Mobile don't buy enough spectrum in enough markets, they will be forced to be a pure voice and sms seller. Verizon and Cingular will know the T-Mobile weak spots and poor coverage: they will fight to keep the weak spots weak and thereby keep T-Mobile weak.

Sprint Nextel is someone who I believe isn’t really interested in this auction, mainly because of bigger internal challenges. I think the process is being driven by TimeWarner and Comcast. I expect to see SpectrumCo (the name of their JV) to bid strongly in the markets where the cables companies have licenses, so if the holy grail of triple and quad plays actually work they have spectrum to fight AT&T/Cingular and Verizon without all of the proceeds going to Sprint Nextel.

The most intriguing bidder is DirectTV, EchoStar and LibertyOne aka Wireless DBS. As we see from exploits of Murdoch in the UK via BSkyB – satellite is going interactive and I think Auction 66 is one of the few possibilities of having a return path in the USA. I suspect if successful, the whole US Satellite industry will be restructured and the inclusion of John Malone’s LibertyOne signals to me that they are prepared to bid more than DirectTV and EchoStar could afford together. The placing of a near US$1bn deposit signals to everyone that this partnership is serious and going to bid strong.

That is enough players to ensure that the Regional mega-licenses are sold for a lot of money: Verizon, Cingular, T-Mobile and Wireless DBS cannot carve up 4 nationwide licenses when there are only 3 on offer.

In addition in huge auctions there are always silent players sat on sidelines waiting for an opportunity. An example of this was the huge bidding in the UK 3G auction by TIW of Canada which remained a mystery until it was revealed that Hutchison of Hong Kong were behind them. There will be plenty of wireless arbitragers sat on the sidelines, watching and willing to buy a seat on the table in the middle of the poker (oops sorry auction) game if necessary.

Smaller License Areas

One of the great things about the US auctions is the amount of players who are willing to risk a lot of capital, including the major players named above there are 168 bidders qualified: 9 have placed deposits over US$100m; 8 have placed deposits between US$80m and US$10m; 30 have placed deposits between US$10m and US$1m; and 121 less than US$1m.

For instance, Leap Wireless aka Cricket have placed a deposit of US$255m on the auction. Leap Wireless specialise in building low cost networks in smaller cities - that is a big deposit for purely small cities. Perhaps they have a mystery backer for moving into the bigger cities?

In fact, there are professional players in the US Auctions who are basically just shopping for bargains to be later re-sold. The existence of these players is enough to ensure that prices are kept high. There is more than enough bidders to keep the bidding even on the smaller licenses fair and square. In we add into the equation that the majors will want to keep minor players out of the Top 100 markets means bidding will be fierce even on the blocks A-C.

No-one wants 3G services

I’ve heard more than a couple of people say 3G services are a big disappointment and therefore no-one will bid a lot for the licenses.

The truth is that Verizon have just reported that their quarterly non-SMS data has climbed above US$500m per quarter and that by my calculation Free Cash Flow was about US2bn in the first six months of the year. Cingular have also just reported record profits. That is a lot of profit both to go after and more importantly to protect.

Cellular Companies learnt from the UK Auctions not to overpay

Total Rubbish – for evidence, look at the recent auction of some African assets.

The US government estimates that they will receive around US$15bn from the auction – that is a real low figure and if this is all they receive the Big Cellular companies will be extremely happy. After all, it is just 4 years of Free Cash Flow for Verizon: in other words Verizon could buy every single license on offer and without any additional sales will be in the money after 4 years of a 15 year license.

The reason that auctions realise a lot of money is from the auction design – a lot of people with a lot of money and a lot to lose need to compete for a scarce resource.

That is the environment with Auction 66 and I’ll be extremely surprised if in a couple of week’s time everyone (apart from me) isn’t amazed at the prices being discussed.

US$30bn is the minimum I’m expecting…

<< Home