Murdoch Musings On Broadband

There is a fascinating interview in the recent edition of Time magazine about the WSJ acquisition process, but a particular paragraph stood out for me:

Now look at the recent Q1 estimate of UK Advertising Spend:

The surge in internet spending in incredible and while I am the first to admit that the growth cannot go on for much longer at these levels it certainly is impressive.

Even more impressive is when we look at the Google UK revenues which were £290m (US$578m) in Q1 2007 compared to £171m (US$343m) in Q1 2006 a y-o-y growth rate of 70%. Remember this is before the DoubleClick acquisition and accounts for a huge 45% of UK Internet Ad market if the WARC estimates are correct.

No wonder the Murdoch empire is scheming of ways to take traffic off the Google platform and onto his - witness the recent launch of MySpace.tv as direct competition to YouTube. Also, it will be extremely interesting to follow the BSkyB acquisition strategy in internet content rather than access. The acquisitions of 365Media, MyKindaPlace and the Aura Sports Ad Sales Agency together with the Google alliance and the beefed up SkyNews site are a very interesting start.

When Murdoch talks about the future of newspapers, you get a sense of how contemporary he really is. Circulation and advertising revenues are ebbing away everywhere, he notes, proportional to broadband penetration. "You've really got to worry," he says. "Tribune Co.'s revenues [in May] dropped 11% across broadcasting and newspapers. That's huge. The Times dropped 8.5%. Half of men under 30 aren't reading print newspapers, and there's no sign that they come back as they age."If you think about the Murdoch Snr musings on broadband, you can see immediately why Murdoch Jnr is investing huge sums on developing a broadband future in the UK.

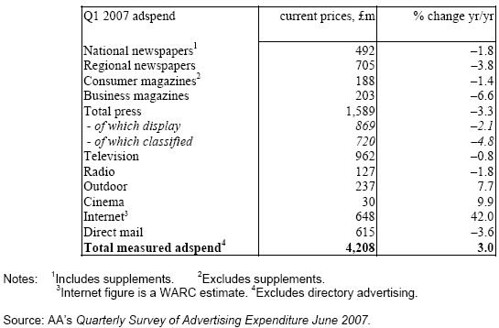

Now look at the recent Q1 estimate of UK Advertising Spend:

The surge in internet spending in incredible and while I am the first to admit that the growth cannot go on for much longer at these levels it certainly is impressive.

Even more impressive is when we look at the Google UK revenues which were £290m (US$578m) in Q1 2007 compared to £171m (US$343m) in Q1 2006 a y-o-y growth rate of 70%. Remember this is before the DoubleClick acquisition and accounts for a huge 45% of UK Internet Ad market if the WARC estimates are correct.

No wonder the Murdoch empire is scheming of ways to take traffic off the Google platform and onto his - witness the recent launch of MySpace.tv as direct competition to YouTube. Also, it will be extremely interesting to follow the BSkyB acquisition strategy in internet content rather than access. The acquisitions of 365Media, MyKindaPlace and the Aura Sports Ad Sales Agency together with the Google alliance and the beefed up SkyNews site are a very interesting start.