Verizon Wireless v T-Mobile USA: Size does Matter

There is an urban myth that size doesn’t matter: this is extremely easy to disprove in the case of the US Cellular Industry and a quick peep at the Verizon Wireless and T-Mobile USA 3Q results illustrates the point.

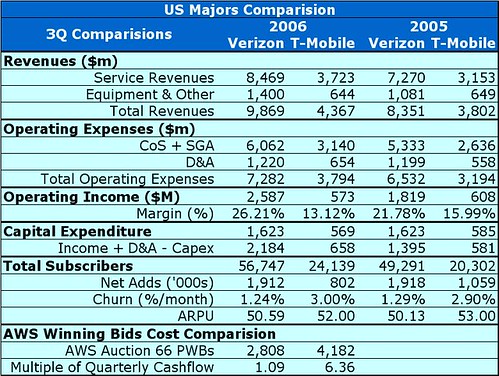

Comparing the T-Mobile 3Q 2006 KPI’s to Verizon Wireless:

If we look at year-on-year comparisons:

This spells real difficulties for the parent company of T-Mobile USA, Deutsche Telekom, because the USA cellular operations have been the engine of growth over the last couple of years. In contrast, Verizon Wireless is providing plenty of growth for Vodafone, the Verizon Wireless debt load is rapidly declining and most importantly the day when the distribution of substantial dividends are restarted is probably only 18 months away.

Comparing the T-Mobile 3Q 2006 KPI’s to Verizon Wireless:

• User base is around 42%;T-Mobile is only delivering a quarter of the profits of Verizon Wireless. It is easier to compare T-Mobile and Verizon Wireless because both companies only use one network technology whereas Cingular and Sprint currently have multiple network technologies.

• Service Revenue is around 44%;

• Operating Profit is around 22%; and

• Capex is around 35%

If we look at year-on-year comparisons:

• Subscribers – Verizon 7.4m, T-Mobile 3.8mAlthough the % growth in T-Mobile subscribers and service revenues is greater than the relevant Verizon figures, the absolute figures are actually dwarfed. In operating profit, T-Mobile USA has actually gone into decline and I’m sure this is because it is becoming more and more expensive to compete against Verizon (and Cingular). Even worse is the amount of investment T-Mobile has had to make into spectrum via Auction 66 and this is before the expense of a national build-out. I’m sure this extra investment was the reason that T-Mobile could claim a non-cash US$1.5bn tax gain below the operating income line.

• Service Revenues – Verizon US$1.2bn, T-Mobile US$0.6bn

• Profit – Verizon US$768m, T-Mobile US$-35m

This spells real difficulties for the parent company of T-Mobile USA, Deutsche Telekom, because the USA cellular operations have been the engine of growth over the last couple of years. In contrast, Verizon Wireless is providing plenty of growth for Vodafone, the Verizon Wireless debt load is rapidly declining and most importantly the day when the distribution of substantial dividends are restarted is probably only 18 months away.

<< Home