3Q2006: Broadband Britain State of the Nation

Most of the major players have now reported:

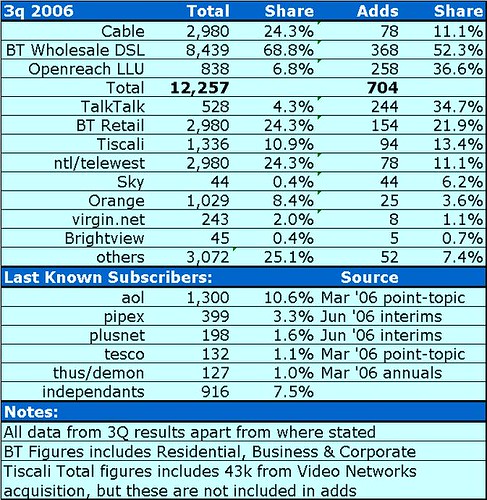

I was really surprised with the press comments today that BT Retail was a loser in 3Q: I’ve actually got them down as a big winner, especially if they are selling the majority of their subscriptions to top end packages as was claimed in the results conference call. I really think that BT Retail is starting to differentiate themselves as a premium provider.

Tiscali also reported last night and again they are adding beyond their market share and this is before the 43k subscribers from the HomeChoice acquisition. Tiscali continue to surprise me.

I refuse to say it was a successful quarter for TalkTalk, because although they took the market by storm in terms of market share, it is not good to be launching with such a poor reputation.

Orange had a dire quarter especially if you consider that they launched their “free broadband” offer. I wonder if they have taken their eyes off the ball as Orange and Wanadoo have been merged.

The other nightmare quarter was for ntl / telewest and I think we are now seeing the weakness of their coverage. I suspect this is the rationale behind their plan of building Virgin.net into a substantial off-net presence.

Of the non-reporters, I suspect that AOL also had a bad quarter. TalkTalk are forecasting 1.5m broadband customers at completion of the acquisition which will mean that AOL will have added around 200k in 9 months. This is well below their total market share.

Pipex will shoot up the table with the 120k or so customer acquired from C&W - Bulldog.

It is also significant how small the “independent” pie is becoming in the overall market – notice that this is not just the independent market, but also the SME & Corporate market. In the next quarter, I also suspect some more M&A activity will go on with perhaps Demon and PlusNet being hoovered up.

I was really surprised with the press comments today that BT Retail was a loser in 3Q: I’ve actually got them down as a big winner, especially if they are selling the majority of their subscriptions to top end packages as was claimed in the results conference call. I really think that BT Retail is starting to differentiate themselves as a premium provider.

Tiscali also reported last night and again they are adding beyond their market share and this is before the 43k subscribers from the HomeChoice acquisition. Tiscali continue to surprise me.

I refuse to say it was a successful quarter for TalkTalk, because although they took the market by storm in terms of market share, it is not good to be launching with such a poor reputation.

Orange had a dire quarter especially if you consider that they launched their “free broadband” offer. I wonder if they have taken their eyes off the ball as Orange and Wanadoo have been merged.

The other nightmare quarter was for ntl / telewest and I think we are now seeing the weakness of their coverage. I suspect this is the rationale behind their plan of building Virgin.net into a substantial off-net presence.

Of the non-reporters, I suspect that AOL also had a bad quarter. TalkTalk are forecasting 1.5m broadband customers at completion of the acquisition which will mean that AOL will have added around 200k in 9 months. This is well below their total market share.

Pipex will shoot up the table with the 120k or so customer acquired from C&W - Bulldog.

It is also significant how small the “independent” pie is becoming in the overall market – notice that this is not just the independent market, but also the SME & Corporate market. In the next quarter, I also suspect some more M&A activity will go on with perhaps Demon and PlusNet being hoovered up.

<< Home