UK Fixed Line Call Revenues

There was some interesting data in the detail of the Q1 2006 Data Set released recently by OFCOM.

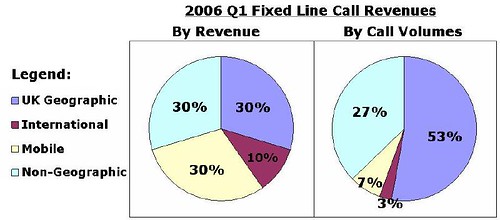

One was the share of revenue by call type compared to traffic volume. Obviously the effects of “bundled” geographic call packages are kicking in and the highest revenue earner is for fixed companies is in fixed-mobile call revenue. 60-70% of fixed line call revenue are “outside” of the typical bundle and this provides plenty of additional revenue for the bundlers to aim at. You can also see the appeal to Orange, Vodafone and O2 of bringing this revenue on-net and therefore having a big advantage compared to non-mobile players such as TalkTalk, Tiscali and AOL - BT is a different story.

The above relates purely to Call Revenue which was £1,367m for the quarter and excludes Access Fees which are now at £1,129m. Given current trends, I think within a couple of years access fees will be higher than call revenue in the fixed market and possibly are already if you consider a “bundle” as a fixed fee. The split between residential (£1,528m) and business revenues (£942m) also shows the folly of building a network to support just the residential market – every operator needs the business traffic to fill its’ pipes 24/7 and not just in the evening period.

The other interesting story in the statistics is in the mobile arena with the lack of revenue growth at both Vodafone and Orange compared to the relatively stellar growth of o2 and T-Mobile. If Vodafone isn't careful, they will be losing their #1 market position in terms of revenue to o2 very soon. Vodafone are already rated as #4 in terms of subscribers. This probably accounts for their recent re-emergence in the consumer market.

Although not especially up-to-date, OFCOM provides the best and most “consistent” statistics which and still is the #1 source for historical analysis of the various communications markets.

One was the share of revenue by call type compared to traffic volume. Obviously the effects of “bundled” geographic call packages are kicking in and the highest revenue earner is for fixed companies is in fixed-mobile call revenue. 60-70% of fixed line call revenue are “outside” of the typical bundle and this provides plenty of additional revenue for the bundlers to aim at. You can also see the appeal to Orange, Vodafone and O2 of bringing this revenue on-net and therefore having a big advantage compared to non-mobile players such as TalkTalk, Tiscali and AOL - BT is a different story.

The above relates purely to Call Revenue which was £1,367m for the quarter and excludes Access Fees which are now at £1,129m. Given current trends, I think within a couple of years access fees will be higher than call revenue in the fixed market and possibly are already if you consider a “bundle” as a fixed fee. The split between residential (£1,528m) and business revenues (£942m) also shows the folly of building a network to support just the residential market – every operator needs the business traffic to fill its’ pipes 24/7 and not just in the evening period.

The other interesting story in the statistics is in the mobile arena with the lack of revenue growth at both Vodafone and Orange compared to the relatively stellar growth of o2 and T-Mobile. If Vodafone isn't careful, they will be losing their #1 market position in terms of revenue to o2 very soon. Vodafone are already rated as #4 in terms of subscribers. This probably accounts for their recent re-emergence in the consumer market.

Although not especially up-to-date, OFCOM provides the best and most “consistent” statistics which and still is the #1 source for historical analysis of the various communications markets.

<< Home