Carphone Warehouse: Almost a statement

The CPW trading statement was a real mixed-bag between the various operations, but the real story is that the CEO and founder, Charles Dunstone, is behaving extremely badly and becoming more and more detached from the reality of his fixed-line customers and despite deploying his PR skills to the max will ultimately be exposed as a charlatan.

1) Distribution

Least we forget, but Distribution is the cornerstone of the Dunstone Paper Empire and the only part generating real cash and profits. For FY06 Distribution generated £109m profits (before interest & tax) out of a group total of £87m.

The connections figures look extremely good with an increase in contracts of 266k and pre-paid of 850k. If gross profits have been maintained at circa £100 and £28 respectively then the connections will add £26m to contract and £24m to pre-paid gross profits which is an approx 25% increase y-o-y. This translates to around £16m, if anyone takes any notice of the unique CPW metric of contribution, assuming a steady conversion ratio at just below 30%. The flip side is a 21.1% increase in stores - I’m not sure about the effect on like-for-like sales and furthermore I’m not exactly sure of the relevance of this archetypical retail metric. For instance, how does the launch of the CPW’s fourth major online site, The Phone Spot, with its’ mega-advertising budget fit in with typical store comparisons?

The importance of the Distribution arm cannot be understated and it was noted that Dunstone did not play his usual Santa scripted “Look at the products we have got coming for Christmas” game that is usual part of the interim trading statement. I sensed a chinck in the armour for the forthcoming vital Christmas period: CPW do not seem to have a “blockbuster” exclusive such as the Pink-RAZR equivalent.

Furthermore, I am still amazed that no-one discussed the conflict of interests between his fixed-line positioned and the ambitions of Orange, O2, Vodafone and Virgin Mobile in this segment. This would be especially worrying given the big “independent” mobile retail competitor (P4U) is not playing in the space.

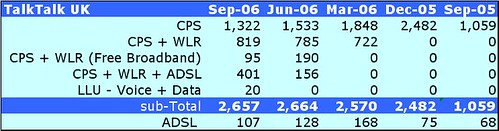

2) Consumer Broadband

When we present the TalkTalk UK figures in a different format to the CPW presentation, we can draw a radically different conclusion – there is no radical growth of the base!

The big spurt in growth was when CPW bought in Dec ‘05:

- One.tel 1.15m CPS customers + 60k ADSL for £132m at around £115/customer. Note there is a £22.2m upside in the price if Centrica manage to sell some customers

- Tele2 214k CPS customers (36k in Ireland) for £10.5m at around £47/customer.

Since then we have effectively seen CPW making a huge investment in infrastructure and pushing the base towards taking line rental and broadband services. We know that WLR on its’ own is effectively a zero margin business and the CPW rationale is that it decreases the churn. We also know that bundle for CPS+WLR+ADSL is loss-making at the gross level. The only area which might be profitable in the long run is LLU where a contribution of £7/customer/month is claimed. The ratio I like is 0.7% of the TalkTalk base is at its’ ultimate destination point. Please bear in mind that the unique CPW contribution metric is before support costs, SAC’s, depreciation of equipment and head office costs.

Please don’t get me wrong, I know that CPW has had people from other networks churning onto its’ network, but I also know that the churners off it’s’ network are in equal measure. The other problem for Dunstone is that theoretically all he is doing is substituting a low-capital consuming reseller base for a high capital consuming network base. Is the risk worthwhile?

3) Customer Service

I think that Charles Dunstone has made a huge PR gaffe with his, frankly, trickery with his appalling customer service.

First of all, he presented a graph showing “calls answered” steadily rising over the weeks to around 250k/week and the average speed to answer declining what looks like sub-1 minute from around 13 minute at peak. Who are making this 250k/week calls – his CPS base? His LLU base? Does it matter if the base is not increasing? The trend is an increase in calls/ overall customer

What is missing from the graph is the number of dropped calls i.e. the calls where the IVR instructs the queue is too long and to call back later automatically terminating the call and where someone has given up and hung up. According to my own limited personal sample: I have called the helplessline 11 times and not got through to an operator 8 times.

Secondly and most disgustingly he presents a chart where he claims that CPW are now in the top-tier of response times. If I was an executive of BT, NTL, Orange or Tiscali, I would be going ballistic given that CPW auto-drop calls and not have revealed anything of statistical significance about the survey. It is definitely a case of saying “We are crap and I won’t reveal who is crapper than us, but nudge-nudge isn’t it time that WatchDog pick on someone else than us” – pathetic.

Thirdly, what is the relevance of the “time elapsed taken to pick up the phone” to customer service? How about if when you finally get through they tell you a bunch of lies and try and blame someone else (even the modem manufacturer) for their incompetence and then charge you for the pleasure? If I was the CEO of OpenReach I’d be now setting up a simple lie-detection test – every time equipment fails in the exchange, I’d ring up the relevant customer service line and wait for them to blame BT, never OpenReach. It is always BT’s fault and shock horror they will charge you £70 if you dare to report an incorrect fault. These despicable tactics (aka call centre scripts) are surely driven by some call centre supervisor on instruction from someone on high – “Pretend we are the people’s champion and everyone else is rubbish and hope we had a bunch of idiots as users”

Finally, and I think this was a Freudian slip by Dunstone, was when he mentioned that people still kept in the queue despite the length and quality because of the value of the deal. Yes, TalkTalk are a bargain basement service currently losing tons of money attracting the people wanting a bargain. These are exactly the type of people who just love to churn and personally I have counter displaying days to go before churn every time I connect to TalkTalk Broadband

4) Missing Operations

We are missing comments on the German Phone House MVNO business, where every man and his dog knows a vicious price war is taking place in the low-end market segment where CPW position itself. We are missing a comment on the perennial loss making UK Fresh & MobileWorld MVNO operations. Similarly we are missing comment on press speculation that MVNO launches are planned in Portugal and Spain. Personally, I’m not expecting fantastic progress.

We are also missing comments on the progress of the Opal Telecom B2B business, where every other altnet is reporting competitive pressures in the UK market.

Finally, we are missing comments on the Dealer business, which strangely enough is also perennially loss-making and has undergone a radical restructure with the purchase of Hugh Symons wholesaling operation and the recruitment of Stuart Henry - ex-Orange Indirect Chieftain who seemed to specialize in winding-up all the independent sector which are now his customers.

5) AOL acquisition

I have a gut feel that this is going to be a really problematic acquisition for CPW on several fronts:

- Customer Base: the average AOL customer is not your typical discount TalkTalk punter. They are technically proficient early-adopters, whereas TalkTalk are playing for the technically challenged mass-adopters. Churn will be a problem;

- Marketing: CPW have already said they are going to slash the “above-the-line” marketing budget. New customers to AOL will dry up;

- Technical Staff & Infrastructure: AOL knows how to run an ISP, TalkTalk don’t have a clue. TalkTalk need the AOL staff technical skills more than they can admit. I have a suspicion that the AOL staff will not find a sympathetic shoulder to cry on and therefore will not hang around for too long.

- Dual Branding: given TalkTalk’s incompetence on simple thing like DNS services, I can’t imagine how things like email hosting, portal sharing and ad-networks are going to work. I predict a huge fall-out.

On numbers and value, I’ll have to look at tomorrow.

6) Overall

In the trading release, Charles Dunstone cryptically said that he expected “interim headline pre-tax profits, before broadband and Virgin Mobile France operations” to be up by 50%. Pre-tax interim profits in 2005 was £32.5m and a 50% uplift gives £49m. However, total losses for Virgin Mobile in FY07 are estimated at £10m and with today’s revised estimate of broadband losses at £70m and with the losses estimated to be skewed towards the first half – I wonder if Carphone Warehouse will enter the realm of post-tax losses?

Dunstone said tonight in a sycophantic interview on BBC Radio4 that he expected that TalkTalk would be seen as the #1 alternative to BT in the future. Personally, I feel Dunstone is nothing more than an “all fur coat and no knickers” chappie that was doing limited damage when acting as a pure retailer, however now he can inflict some serious damage to the UK economy if a significant proportion of population was reliant on his terrible service. Ultimately, it would be a horror show if the “UK digital divide” was those people who used the “Charles Dunstone” service and those who didn’t.

1) Distribution

Least we forget, but Distribution is the cornerstone of the Dunstone Paper Empire and the only part generating real cash and profits. For FY06 Distribution generated £109m profits (before interest & tax) out of a group total of £87m.

The connections figures look extremely good with an increase in contracts of 266k and pre-paid of 850k. If gross profits have been maintained at circa £100 and £28 respectively then the connections will add £26m to contract and £24m to pre-paid gross profits which is an approx 25% increase y-o-y. This translates to around £16m, if anyone takes any notice of the unique CPW metric of contribution, assuming a steady conversion ratio at just below 30%. The flip side is a 21.1% increase in stores - I’m not sure about the effect on like-for-like sales and furthermore I’m not exactly sure of the relevance of this archetypical retail metric. For instance, how does the launch of the CPW’s fourth major online site, The Phone Spot, with its’ mega-advertising budget fit in with typical store comparisons?

The importance of the Distribution arm cannot be understated and it was noted that Dunstone did not play his usual Santa scripted “Look at the products we have got coming for Christmas” game that is usual part of the interim trading statement. I sensed a chinck in the armour for the forthcoming vital Christmas period: CPW do not seem to have a “blockbuster” exclusive such as the Pink-RAZR equivalent.

Furthermore, I am still amazed that no-one discussed the conflict of interests between his fixed-line positioned and the ambitions of Orange, O2, Vodafone and Virgin Mobile in this segment. This would be especially worrying given the big “independent” mobile retail competitor (P4U) is not playing in the space.

2) Consumer Broadband

When we present the TalkTalk UK figures in a different format to the CPW presentation, we can draw a radically different conclusion – there is no radical growth of the base!

The big spurt in growth was when CPW bought in Dec ‘05:

- One.tel 1.15m CPS customers + 60k ADSL for £132m at around £115/customer. Note there is a £22.2m upside in the price if Centrica manage to sell some customers

- Tele2 214k CPS customers (36k in Ireland) for £10.5m at around £47/customer.

Since then we have effectively seen CPW making a huge investment in infrastructure and pushing the base towards taking line rental and broadband services. We know that WLR on its’ own is effectively a zero margin business and the CPW rationale is that it decreases the churn. We also know that bundle for CPS+WLR+ADSL is loss-making at the gross level. The only area which might be profitable in the long run is LLU where a contribution of £7/customer/month is claimed. The ratio I like is 0.7% of the TalkTalk base is at its’ ultimate destination point. Please bear in mind that the unique CPW contribution metric is before support costs, SAC’s, depreciation of equipment and head office costs.

Please don’t get me wrong, I know that CPW has had people from other networks churning onto its’ network, but I also know that the churners off it’s’ network are in equal measure. The other problem for Dunstone is that theoretically all he is doing is substituting a low-capital consuming reseller base for a high capital consuming network base. Is the risk worthwhile?

3) Customer Service

I think that Charles Dunstone has made a huge PR gaffe with his, frankly, trickery with his appalling customer service.

First of all, he presented a graph showing “calls answered” steadily rising over the weeks to around 250k/week and the average speed to answer declining what looks like sub-1 minute from around 13 minute at peak. Who are making this 250k/week calls – his CPS base? His LLU base? Does it matter if the base is not increasing? The trend is an increase in calls/ overall customer

What is missing from the graph is the number of dropped calls i.e. the calls where the IVR instructs the queue is too long and to call back later automatically terminating the call and where someone has given up and hung up. According to my own limited personal sample: I have called the helplessline 11 times and not got through to an operator 8 times.

Secondly and most disgustingly he presents a chart where he claims that CPW are now in the top-tier of response times. If I was an executive of BT, NTL, Orange or Tiscali, I would be going ballistic given that CPW auto-drop calls and not have revealed anything of statistical significance about the survey. It is definitely a case of saying “We are crap and I won’t reveal who is crapper than us, but nudge-nudge isn’t it time that WatchDog pick on someone else than us” – pathetic.

Thirdly, what is the relevance of the “time elapsed taken to pick up the phone” to customer service? How about if when you finally get through they tell you a bunch of lies and try and blame someone else (even the modem manufacturer) for their incompetence and then charge you for the pleasure? If I was the CEO of OpenReach I’d be now setting up a simple lie-detection test – every time equipment fails in the exchange, I’d ring up the relevant customer service line and wait for them to blame BT, never OpenReach. It is always BT’s fault and shock horror they will charge you £70 if you dare to report an incorrect fault. These despicable tactics (aka call centre scripts) are surely driven by some call centre supervisor on instruction from someone on high – “Pretend we are the people’s champion and everyone else is rubbish and hope we had a bunch of idiots as users”

Finally, and I think this was a Freudian slip by Dunstone, was when he mentioned that people still kept in the queue despite the length and quality because of the value of the deal. Yes, TalkTalk are a bargain basement service currently losing tons of money attracting the people wanting a bargain. These are exactly the type of people who just love to churn and personally I have counter displaying days to go before churn every time I connect to TalkTalk Broadband

4) Missing Operations

We are missing comments on the German Phone House MVNO business, where every man and his dog knows a vicious price war is taking place in the low-end market segment where CPW position itself. We are missing a comment on the perennial loss making UK Fresh & MobileWorld MVNO operations. Similarly we are missing comment on press speculation that MVNO launches are planned in Portugal and Spain. Personally, I’m not expecting fantastic progress.

We are also missing comments on the progress of the Opal Telecom B2B business, where every other altnet is reporting competitive pressures in the UK market.

Finally, we are missing comments on the Dealer business, which strangely enough is also perennially loss-making and has undergone a radical restructure with the purchase of Hugh Symons wholesaling operation and the recruitment of Stuart Henry - ex-Orange Indirect Chieftain who seemed to specialize in winding-up all the independent sector which are now his customers.

5) AOL acquisition

I have a gut feel that this is going to be a really problematic acquisition for CPW on several fronts:

- Customer Base: the average AOL customer is not your typical discount TalkTalk punter. They are technically proficient early-adopters, whereas TalkTalk are playing for the technically challenged mass-adopters. Churn will be a problem;

- Marketing: CPW have already said they are going to slash the “above-the-line” marketing budget. New customers to AOL will dry up;

- Technical Staff & Infrastructure: AOL knows how to run an ISP, TalkTalk don’t have a clue. TalkTalk need the AOL staff technical skills more than they can admit. I have a suspicion that the AOL staff will not find a sympathetic shoulder to cry on and therefore will not hang around for too long.

- Dual Branding: given TalkTalk’s incompetence on simple thing like DNS services, I can’t imagine how things like email hosting, portal sharing and ad-networks are going to work. I predict a huge fall-out.

On numbers and value, I’ll have to look at tomorrow.

6) Overall

In the trading release, Charles Dunstone cryptically said that he expected “interim headline pre-tax profits, before broadband and Virgin Mobile France operations” to be up by 50%. Pre-tax interim profits in 2005 was £32.5m and a 50% uplift gives £49m. However, total losses for Virgin Mobile in FY07 are estimated at £10m and with today’s revised estimate of broadband losses at £70m and with the losses estimated to be skewed towards the first half – I wonder if Carphone Warehouse will enter the realm of post-tax losses?

Dunstone said tonight in a sycophantic interview on BBC Radio4 that he expected that TalkTalk would be seen as the #1 alternative to BT in the future. Personally, I feel Dunstone is nothing more than an “all fur coat and no knickers” chappie that was doing limited damage when acting as a pure retailer, however now he can inflict some serious damage to the UK economy if a significant proportion of population was reliant on his terrible service. Ultimately, it would be a horror show if the “UK digital divide” was those people who used the “Charles Dunstone” service and those who didn’t.

<< Home