AWS-1 Bargain or Rip-off

With the AWS-1 Auction winding-up and almost certainly bidding in the Supa-Regional auctions is over, it is worth crystal ball gazing as to whether the bids were too low or too high.

Acquiring spectrum is only one part of the cellular business model, albeit an extremely expensive one on the capital side of the equation. It should be noted that other variable’s such as pricing, usage, equipment costs, operating costs, interest rates & taxation are equally important and not considered in this analysis.

In determining value of spectrum, the most important consideration is the spectral efficiency of the deployed system and of course this is inextricably linked to the chosen technology. I have used the EV-DO roadmap as an example, but please bear in mind some of the technology is already deployed and some is still being worked on in the labs and therefore the results are not guaranteed. The USA is obviously going to be the battle ground to prove which system is the best in practice with WCDMA, EV-DO and Wimax planned to be deployed. As a European Consumer, I wish companies themselves had a vote on the technological winners and losers but currently they have to rely on some decision made by some anonymous bureaucrat and politicians many years before.

Wireless spectrum is obviously shared between authenticated users in a given cell, so on an engineering basis we have to really look at estimated peak-hour usage and cell size in a variety of urban, suburban and rural locations to give an idea of what bandwidth can ultimately be offered in a huge variety of locations.

I expect in the medium term as customers actually start using the AWS spectrum a huge marketing battle developing as to which wireless operator offers the best “quality” speeds. The figures quoted by all equipment manufacturers and standards bodies tend to be theoretical layer-1 speeds (ie physical) rather than figures that have any meaning to users e.g. actual download times (ie application level) or streaming success (ie without pausing for buffering) The 802.11b ratios are roughly about 1:2 for actual vs declared speed and this estimate is before considering congested access points in which performance drops off dramatically. Basically, the whole upcoming confusion is a license to print money for independent assessors.

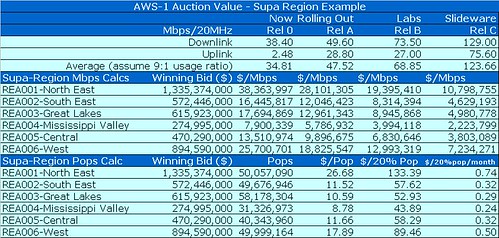

If we look at the spectrum cost on a per population basis, I believe the important point is showing the importance of current market share as a barrier to bidding. For instance, Verizon Wireless bid US$1.335bn for the whole of the North West area. I’m not sure of the market share of VZW in the North East, I’d guess it is actually greater than 20%. At 20% the cost of a 15 year license is US$133/20% pop customer. To me this highlights one of the main reasons why the auction failed to attract a low of bids from new entrants: just because of existing market share the incumbents have developed huge barriers to entry.

The most important variable as far as profitability is concerned is competition. The experience of 3G auctions here in the UK, I believe show that sunk costs (ie auction fees) are immaterial compared to increased levels of competition. At first glance, the AWS-1 auction seems to be a failure on increasing competition.

Acquiring spectrum is only one part of the cellular business model, albeit an extremely expensive one on the capital side of the equation. It should be noted that other variable’s such as pricing, usage, equipment costs, operating costs, interest rates & taxation are equally important and not considered in this analysis.

In determining value of spectrum, the most important consideration is the spectral efficiency of the deployed system and of course this is inextricably linked to the chosen technology. I have used the EV-DO roadmap as an example, but please bear in mind some of the technology is already deployed and some is still being worked on in the labs and therefore the results are not guaranteed. The USA is obviously going to be the battle ground to prove which system is the best in practice with WCDMA, EV-DO and Wimax planned to be deployed. As a European Consumer, I wish companies themselves had a vote on the technological winners and losers but currently they have to rely on some decision made by some anonymous bureaucrat and politicians many years before.

Wireless spectrum is obviously shared between authenticated users in a given cell, so on an engineering basis we have to really look at estimated peak-hour usage and cell size in a variety of urban, suburban and rural locations to give an idea of what bandwidth can ultimately be offered in a huge variety of locations.

I expect in the medium term as customers actually start using the AWS spectrum a huge marketing battle developing as to which wireless operator offers the best “quality” speeds. The figures quoted by all equipment manufacturers and standards bodies tend to be theoretical layer-1 speeds (ie physical) rather than figures that have any meaning to users e.g. actual download times (ie application level) or streaming success (ie without pausing for buffering) The 802.11b ratios are roughly about 1:2 for actual vs declared speed and this estimate is before considering congested access points in which performance drops off dramatically. Basically, the whole upcoming confusion is a license to print money for independent assessors.

If we look at the spectrum cost on a per population basis, I believe the important point is showing the importance of current market share as a barrier to bidding. For instance, Verizon Wireless bid US$1.335bn for the whole of the North West area. I’m not sure of the market share of VZW in the North East, I’d guess it is actually greater than 20%. At 20% the cost of a 15 year license is US$133/20% pop customer. To me this highlights one of the main reasons why the auction failed to attract a low of bids from new entrants: just because of existing market share the incumbents have developed huge barriers to entry.

The most important variable as far as profitability is concerned is competition. The experience of 3G auctions here in the UK, I believe show that sunk costs (ie auction fees) are immaterial compared to increased levels of competition. At first glance, the AWS-1 auction seems to be a failure on increasing competition.

<< Home