UK Subsidy War

One would logically expect exclusives, the best sellers or the phones offering the highest margins to get the highest real estate on the front page. What is interesting is the way the real estate has changed over the last year: first of all, through most of 2005 3UK had almost blanket coverage; then early in 2006, T-Mobile hit back with the launch of its’ Flexr tariff whilst 3UK dropped its’ commissions and tried to discourage cashbacks; and now it looks as if T-Mobile is pulling back on the commissions and being severely warned by the retailers about its’ action.

In my humble opinion, a subtle shift is happening in the UK market: first of all much lower absolute tariffs so the big 4 MNOs compete with 3UK huge buckets; second, extended 18 month contracts to reduce churn; now the push for lower commissions thereby reducing SACs further; and finally I expect a huge effort to push the on-line community into the operators own portals. It will be extremely interesting to see how this trend plays out in the next 12 months of KPIs released by the MNOs, Retailers and Handset Manufacturers.

This on-going battle between operators, retailer and manufacturers is the front line battlefield for the operator dump-pipe avoidance schemes.

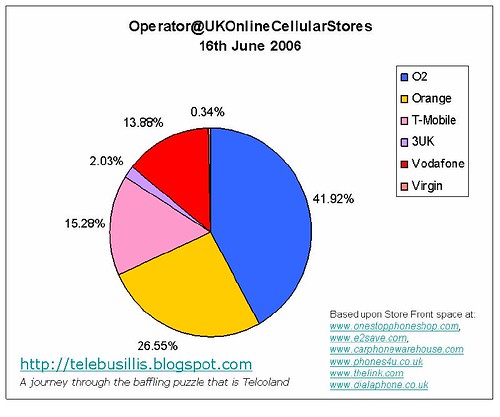

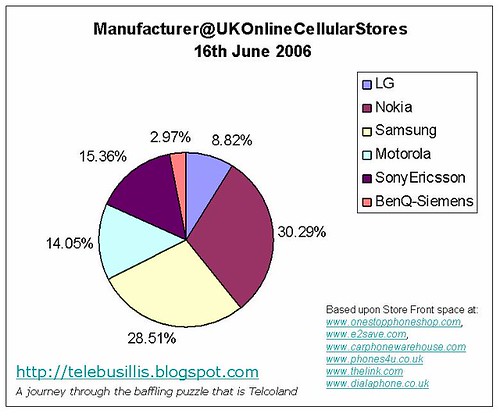

The on-line market is becoming a huge consumer sales channel. CPW itself sold £203.5m online compared to retail of £1,375.5m (across the whole CPWEuroPortfolio). Most of the above analysis is based upon gut feel. In an attempt to be a little more scientific, I’m going to start two new trackers Manufacturer@UKOnlineCellularStores and Operator@UKOnlineCellularStores both of which will cover only the main real estate of the retailers.

<< Home