BT Regulated Accounts for 2006/7: Scary Stuff

The results are finally published and hidden amongst the 126 pages are some potential time bombs for non-BT UK investors.

First, it is becoming apparent why no-one will publicly discuss broadband churn figures and that is because they are straight out of a Hammer Horror Movie:

MPF churn of 33% and assuming a mass migration Openreach charge of £27.54 gives monthly amortization of 75p/customer. If churn increases to 50% and a single standard line transfer for £34.86 is used then this equates to a huge monthly charge of £1.45 which needs to be amortised.

Of course, in some unbundlers accounts this hardly matters because in this “we-have-not-learnt-anything-from-the-tech-bubble” era amortization is below the EBITDA line and therefore does not count in some analyst eyes. In fact, churn is really, really crucial in a capex intensive game and there are far more charges than OpenReach connection charges to be factored in with broadband customer acquisition. In my broadband model, I factor in another £30/connection for marketing and another £10 for CPE, but that was before the era of “free broadband and free laptops”. And that is before the kit, backaul and back-office systems…

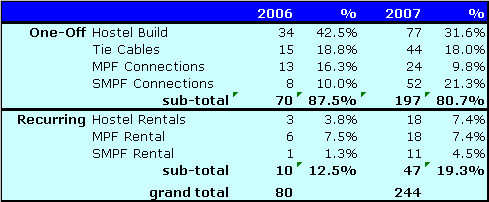

The next interesting snippet from the OpenReach accounts is the breakdown of revenues:

The recurring revenues are currently immaterial compared with the one-off revenues: not for BT the typical customer opex driven hosting model, BT has learnt over the years how to tempt customers into a spending spree with front loading of costs which the customers can capitalize and analysts can pretend they don’t affect the companies valuation.

OpenReach booked 4.4k hostel builds at an average cost of £17.2k and sold 88k tie cables at £500/100 copper pairs. When an unbundler abandons its retail strategy and decides to sell wholesale with a customer whose territory has a huge overlap with your unbundled area, it can’t be long before a huge write-off and loss of face is about to be forthcoming.

Even more interesting is that OpenReach is earning £3k/annum rental for the average hostel – it is pretty obvious that at the current low utilization rates the unbundlers need to scale fast. A certain marketing driven mobile operator plans to have the least aggressive approach to marketing broadband in the history of consumer launches whilst at the same time having a large exchange footprint - this is going to cost it dearly in ongoing losses. In fact, when the Post Office has more aggressive broadband marketing plans than the mobile operator, it just goes to show how rapidly someone can lose their mojo.

There is another line is the OpenReach accounts which is of interest to the unbundlers and that is the metro Ethernet business which is predominately used for broadband backhaul:

Here the breakdown of connections in 2006/7 is revealing:

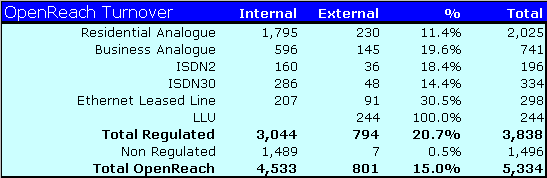

On a more serious note it is important to note that most of regulated revenues of OpenReach still is generated from 20th century analogue copper pipes. And most importantly there is only 10% (switching and transmission) of the asset base which could claim to be acquainted with Moores Law.

This last graphic should send shivers down the spine of every unbundler in the country and that is because OpenReach are declaring only an 8% return on mean capital employed; OFCOM guaranteed them a 10% return on the “Regulated Asset Value”. A mere £187m of profit shortfall.

I am 100% sure that there are definitional differences between the OpenReach 8% and the OFCOM 10%, but the fact of the matter is that BT have an obligation to their shareholders to get the required 10% return and if 1990s history is anything to go by can argue for years and years proving their point. I will need a lot more time and motivation to examine where the real differences are and the potential area where BT will look to raise prices.

However, I believe all this is just a mark in the sand from BT , before the debate over 21CN expenditure really kicks in… and we are entering a period where as a country unfortunately we need to grovel to BT to get FTTH rolled out… and even worse OFCOM is still gloating in the apparent regulatory brilliance of the creation of OpenReach and is busy running to Brussels saying how it is a model which needs to be forced on the rest of Europe. Meus Deus...

It is going to be a difficult couple of years for the unbundlers and I would advise them to hire some regulatory specialists and political lobbyists as soon as possible...

Hat Tip: YKWYA

First, it is becoming apparent why no-one will publicly discuss broadband churn figures and that is because they are straight out of a Hammer Horror Movie:

MPF churn of 33% and assuming a mass migration Openreach charge of £27.54 gives monthly amortization of 75p/customer. If churn increases to 50% and a single standard line transfer for £34.86 is used then this equates to a huge monthly charge of £1.45 which needs to be amortised.

Of course, in some unbundlers accounts this hardly matters because in this “we-have-not-learnt-anything-from-the-tech-bubble” era amortization is below the EBITDA line and therefore does not count in some analyst eyes. In fact, churn is really, really crucial in a capex intensive game and there are far more charges than OpenReach connection charges to be factored in with broadband customer acquisition. In my broadband model, I factor in another £30/connection for marketing and another £10 for CPE, but that was before the era of “free broadband and free laptops”. And that is before the kit, backaul and back-office systems…

The next interesting snippet from the OpenReach accounts is the breakdown of revenues:

The recurring revenues are currently immaterial compared with the one-off revenues: not for BT the typical customer opex driven hosting model, BT has learnt over the years how to tempt customers into a spending spree with front loading of costs which the customers can capitalize and analysts can pretend they don’t affect the companies valuation.

OpenReach booked 4.4k hostel builds at an average cost of £17.2k and sold 88k tie cables at £500/100 copper pairs. When an unbundler abandons its retail strategy and decides to sell wholesale with a customer whose territory has a huge overlap with your unbundled area, it can’t be long before a huge write-off and loss of face is about to be forthcoming.

Even more interesting is that OpenReach is earning £3k/annum rental for the average hostel – it is pretty obvious that at the current low utilization rates the unbundlers need to scale fast. A certain marketing driven mobile operator plans to have the least aggressive approach to marketing broadband in the history of consumer launches whilst at the same time having a large exchange footprint - this is going to cost it dearly in ongoing losses. In fact, when the Post Office has more aggressive broadband marketing plans than the mobile operator, it just goes to show how rapidly someone can lose their mojo.

There is another line is the OpenReach accounts which is of interest to the unbundlers and that is the metro Ethernet business which is predominately used for broadband backhaul:

Here the breakdown of connections in 2006/7 is revealing:

- 100 meg – 1,854 connections

- 1 gig – 833 connections

- Other – 117 connections

On a more serious note it is important to note that most of regulated revenues of OpenReach still is generated from 20th century analogue copper pipes. And most importantly there is only 10% (switching and transmission) of the asset base which could claim to be acquainted with Moores Law.

This last graphic should send shivers down the spine of every unbundler in the country and that is because OpenReach are declaring only an 8% return on mean capital employed; OFCOM guaranteed them a 10% return on the “Regulated Asset Value”. A mere £187m of profit shortfall.

I am 100% sure that there are definitional differences between the OpenReach 8% and the OFCOM 10%, but the fact of the matter is that BT have an obligation to their shareholders to get the required 10% return and if 1990s history is anything to go by can argue for years and years proving their point. I will need a lot more time and motivation to examine where the real differences are and the potential area where BT will look to raise prices.

However, I believe all this is just a mark in the sand from BT , before the debate over 21CN expenditure really kicks in… and we are entering a period where as a country unfortunately we need to grovel to BT to get FTTH rolled out… and even worse OFCOM is still gloating in the apparent regulatory brilliance of the creation of OpenReach and is busy running to Brussels saying how it is a model which needs to be forced on the rest of Europe. Meus Deus...

It is going to be a difficult couple of years for the unbundlers and I would advise them to hire some regulatory specialists and political lobbyists as soon as possible...

Hat Tip: YKWYA