Hutchison Whampoa (HWL)

released its interim results this week and the obvious conclusion is that the 3 Group is still eating cash, albeit at a slower rate than last year. I estimate the ballpark cash outflow at £676m versus £1,268m last year.

The Sunday Times have today tried to explain the harsh realities facing Hutchison 3G, but I think it is extremely difficult to draw any conclusions due to what I consider persistent “extreme KPI gaming” and I think it is more fun to play – spot the games.

Game 1 – Customer Figures

HWL seem to have a reporting cycle all of its’ own – the customer figures are the number registered on the day before the results are released rather than the closing figure for the reporting period. For example in the six months to 30th June 2006, released on the 24th August, the customer numbers relate to the 23rd August rather than the traditional 30th June.

I also note that The Sunday Times quoted an internal source saying that as many as 40% of 3 UK prepaid customers are inactive. H3G UK has certainly had a torrid time in the prepaid segment and I’m sure that today they are wishing they never bothered with the segment.

The net effect of this is that comparisons are impossible to make across the sector. Also standard “per customer” ratio’s for the 3 Group are impossible.

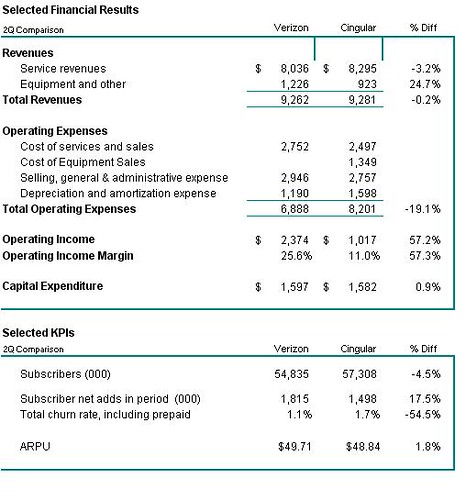

Game 2 – No Churn Percentages

The 3 Group does not release churn percentages: there have been several rumours during the year of huge figures for 3 churn in the UK as high as 60%. HWL seems to have addressed this problem by stating that “churn for the first-half was higher than expected…churn has been progressively reduced and was approx. 3.6% for the month of July”

It was obvious to me right from the start of the huge push in 2004 that 3 UK would have a huge problem with churn. I thought the problem was that effectively 3 UK were giving away a handset and a huge bucket of minutes and texts for “free” over the contract length. Even worse was the mechanism that 3 choose to give away the “free” service which was via a “cashback” mechanism, thus allowing 3 UK to book revenues and booking the discount in the “customer acquisition cost” line. This was a recipe was charlatans and crooks to enter the industry and for extremely dissatisfied customers. It is hardly surprised that recently 3UK have been making noises about building its’ own distribution channel.

Game 3 – New Definitions of Profitability

I know a few accountants who think EBITDA is quite a controversial measure of profitability when used as a valuation metric, because it doesn’t reflect depreciation and amortization charges. Every accountant I know thinks “EBITDA before Customer Acquisition Costs” is a total travesty as a serious metric. HWL dreamed up “EBITDA before Customer Acquisition Costs”.

The only positive about the HWL definition is that it places a focus on the importance of Customer Acquisition Costs on overall profitability. For instance, the 3 Group spent approx. £210m on acquiring prepaid customers in the first six months despite saying that they are not that interested in this segment. Given that total prepaid revenues for the six months were £473m – customer acquisition costs represent a huge percentage (44%). Net prepaid customer numbers grew around 500k in the six months (assumption subject to game 1 trickery) giving a net cost for a prepaid add of £420. For a normal operator who releases churn figures we would be able to work out the % relating to growth (ie net adds - 500k) and the % relating due to ongoing business (replacing churners) with HWL we are clueless and therefore the cynics assume the worst.

Game 4 – Ridiculous ARPU Figures

It only takes a little look at the UK prepaid figures to realize how ridiculous the 3 Group figures are: the UK& Ireland had prepaid revenues of £66.665m, given that there is no growth in the subscriber numbers over the period and the prepaid customer numbers were 1.57m on the 22nd March then in the six months the ARPU was approx. £7.07. The published ARPU (in the trailing twelve months) was £15.49. There is obviously a huge game going on here.

Given the huge percentage discrepancy above and the fact that 3 ARPU’s are declared before promotional discounts, I don’t trust the figures at all, even with the huge incoming interconnect charges. The sudden increase of 20% in UK APRUs should be seen in this context.

In my opinion, the only innovation that 3 has introduced in the UK is the concept of “cashback” and I believe this is the most self-destructive pricing policy ever designed encouraging dubious distributors and fraudulent schemes. “Cashback” schemes fit perfectly into the HWL business model of ignoring acquisition costs and churn.

Game 5 - Non-Voice Revenues

It is almost impossible given the fog of war relating to “cashbacks” and the bundles on offer by 3 UK to have any faith in the non-voice revenue percentages.

For instance, currently the Music & Talk & Text 700 offer has been reduced from £37.50 to £18.75pm for a 12 month contract, in this deal is:

• 400 mins x-network voice (non-geographical extra)

• 250 texts

• 25 UK Video call minutes

• 25 Picture/Video messages

• 5 Music Track downloads

• FREE internet surfing powered by Yahoo! Search

What is the percentage of data revenues in this bundle?

Furthermore, the music companies who are including “free” music in the bundle are running a big risk of devaluing their “download” product, in much the same way that 3G UK has created a problem with the quality of their customer base by giving away service. However, the music companies are well known for their lack of foresight and nothing surprises me about them. You would have thought that with the music industries current problems of illegal “free” downloads; they would not be supporting another “free” scheme.

Game 6 – Capital Expenditure

I was extremely surprised with the level of Capex in the 3 operation - £289m for the six months, down from £474m in the previous year. This seems extremely low to me for a company that should still be building out its’ network in the UK, Ireland, Italy, Sweden, Denmark, Austria and Australia and adding new services (eg HSDPA). For a comparison, Vodafone across the whole of 2005/6 spent £665m in the UK and £541m in Italy.

Two main conclusions can be drawn from this, either:

1. HWL are constraining Capex to improve cashflow figures; or

2. Vodafone are overspending.

I have a little sympathy with both of these answers and there is probably a grain of truth in both. Vodafone capitalize a lot of internal work on IT systems and Network Design and Build to be written off during many years below the EBITDA line in the “Depreciation” line of the accounts, thereby “hiding” a lot of staff costs.

There is a third more potentially harmful conclusion and this relates to the mega-outsourcing deal done with Ericsson in the UK, Italy & Australia for IT and Network Operations. I’ve been thinking that perhaps some of these outsourcing deals in general are done on a “PFI”-type basis, which really is just another expensive type of off-balance sheet funding. This would fit in with some of Ericsson declarations that profits were not as high because of the timing of large outsourcing deals in their results. I would think this type of deal to be reflected in contingent liabilities, but I can’t see any signs in the HWL accounts, so perhaps my fears have no basis. I really hope that my thoughts are incorrect and this is not a growing trend in the industry: I can still remember the difficulties caused by vendor-financing of network builds in the bubble years.

Game 7 – Purchase / Sale of Assets

When the 3 Italia IPO failed in February, HWL announced that it had sold 10% of the company privately to a group of private investors which valued the company at €9bn. It also revealed that with the deal came an option to sell-back the stake to HWL. Now, it is revealed that this deal has to be treated as debt under Accounting Standards and therefore not a sale at all. Personally, I think the transaction was more about saving face than realizing value in the 3G subsidiaries.

Conclusion

It seems at first glance that things are improved albeit slower than the targets that HWL set. However, given the games the HWL seem to play personally I don’t believe a word or number that HWL publish relating to the 3 Group operations.