NANOG people are basically the people who run the internet on a day-to-day basis, so their opinions count for a lot in my book. They have just had their

37th meeting in San Diego and came up with a couple of gems - well, at least to me…

A guy from YouTube gave a short presentation and revealed some extremely interesting facts:

- YouTube serves over 50 million videos a day

- It is growing at approx 20% per month

- Its outbound traffic is 20Gb per second.

This is incredible traffic for a company that has only been in existence for a year. It is hardly surprising that YouTube were basically looking for peering suppliers.

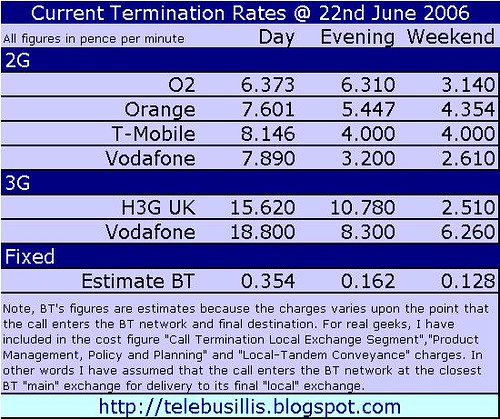

The guru of peering, Bill Norton from Equinix, runs an annual survey of peering costs and from the last conference estimates that average peering costs are $25/Mbps with a high of $95Mbps and a low of $10Mbps. Obviously, the cost seems to be proportional to the size of the pipe.

Using the above as a guide, this means that YouTube’s ISP connectivity costs are theoretically in the order of US$512k/month for each 20Gbps connection. This will rise to US$3.8m/month for 148Gbps in one years time if traffic growth continues at the current pace. That is a lot of adverts required to make the service economic and this is before computing, power and engineering costs. Obviously YouTube will get a discount for bulk, but it provides an insight into the murky world of peering and shows a real world example of the type of connectivity costs that content providers face and the sort of revenues that the Tier1 ISP’s are earning.

Even more interesting is a set of predictions for 2010 that Bill Norton seems to think resonated amongst a couple of dozen ISP attendees.

"We are sitting around this table in 2010 at NANOG and we are commenting how remarkable the last few years have been, specifically that:"

1. We have 10G network interface(s) on laptops (I assumed wired, but someone else might have been thinking wireless)

2. $5/mbps is the common/standard price of transit (other prediction was $30/mbps)

3. Internet traffic is now so heavily localized (as in 75% of telephone calls are across town type of thing but for the Internet)

4. Ad revenue will cover the cost/or subsidize significantly of DSL

5. 90% of Internet bits will be video traffic

6. VoIP traffic exceeds the PSTN traffic

7. Private networks predominantly migrate to overlays over the Internet

8. Wireless Internet Service Providers (WISPs) are serious competitive threat to DSL and Cable Internet

9. Sprint is bought by Time Warner

10. Cable companies form cabal & hookup with Sprint or Level 3

11. Government passes Net Neutrality Law of some flavor

12. Earthlink successfully reinvents themselves as Wireless Metro player in Response to ATT and Verizon

13. 40% paid or subscription as opposed to Content Click Ads. Like Cable Company channel packages, folks will flock to subscriptions for Internet Content packages.

14. RIAA proposes surcharge on network access (like Canada tax on blank CDs)

15. NetFlix conversion to Internet delivery of movies to Tivo or PC, or open source set top box

16. ISPs will be in pain

17. Last mile (fiber, wireless, .) in metro will be funded by municipal bonds

18. Death of TV ads, Death of broadcast TV, Tivo & Tivo like appliances all use the Internet with emergence of targeted ads based on demographic profiles of viewer

19. Google in charge of 20% of ALL ads (TV, Radio, Billboards, .)

20. Ubiquitous wifi in every metro with wifi roaming agreements

21. Congestion issues drive selective customer acceptance of partial transit offerings

22. IPTV fully embraced by cable cos - VOD - no need for VDR and ala carte video services replace analog frequency

23. Near simultaneous release of movies to the theaters, DVDs for the home, PPV, and Internet download to meet needs of different demographics. (Some get dressed up for theater, others have kids and can't leave home, others wantto watch on the flight to Tokyo - all watch the new release movie at about the same time)

Now there is food for thought...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}