EU Regulation on Cross-Border Products

If Vodafone has a huge Pan-European Network, especially when compared to its’ rivals then why does it not exploit this power as a competitive advantage?

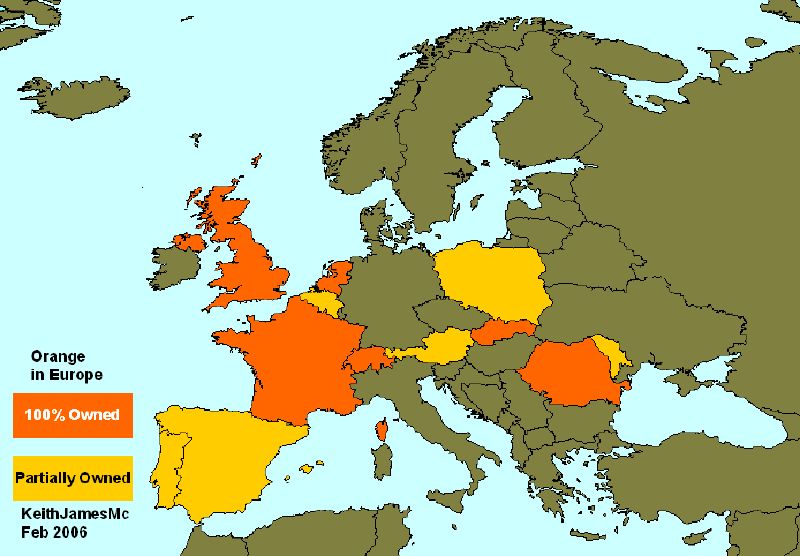

Flashback to April 2000, when VOD bought Mannesmann, there was a wave of complaints to Mario Monti, the EU commissioner at the time that VOD would be able to launch Pan-European services which the other operators would not be able to replicate. What is interesting is that these services, included not only the services that were available at time, such as voice roaming, but also included services that were not available at time such as location based services and corporate LAN access.

The EU also decided that VOD did have a dominant position in any of the services, but could enjoy a time-to-market advantage, because of complexities of negotiating deals for the other operators. In addition to the sale of Orange, Vodafone also undertook for a period of three years to offer the “same price & structure” to competitors if Vodafone lowered its’ Roaming charges.

In other words, Monti nullified any competitive advantage for Vodafone for three years in developing cross-border products & services. It is also interesting that the other operators complained that VOD would become dominant in buying handsets and the competitive advantage was discriminatory, which the commission disagreed with. The complete EU Vodafone/Mannesmann Ruling is here.

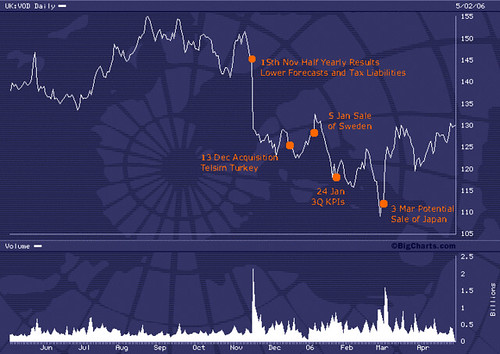

It is hardly surprising then that Vodafone did not launch the Passport product until May 2005. Although, the product targets only voice roaming charges and undoubtedly brings down the charges in a lot of markets, it can hardly be called a cross-border product, since the Pricing, Terms & Conditions vary by country.

Now, we have an ongoing investigation from the EU in roaming charges and the EU seems to now want to get rid of them:

• The new EU regulation should in any event address inter-operator tariffs (wholesale prices). The EU regulation would ensure that operators do not charge operators from other countries substantially more than the actual cost.

• To ensure that operator savings at the wholesale level are actually passed on to the consumer, the Commission sees also a need for regulation at the retail level.

• The new EU regulation could in particular eliminate all roaming charges for receiving a call when travelling abroad in the EU.

• In addition, for calls made while travelling abroad in the EU, the new EU regulation could introduce the “home pricing” principle. A mobile customer travelling abroad in the EU would always be charged only the prices that he is used to paying in his country of residence: he would either pay a local tariff when making a local call, regardless of where he is travelling in the EU (e.g. for calling a cab while travelling in Madrid); or a normal international tariff for calls made to EU destinations, regardless of where he is travelling in the EU (e.g. for calling the family back home while on holidays).

It does not take a genius to conclude that everyone from the largest to the smallest mobile operator will object to these principles. Basically, the EU wants to abolish roaming charges and regulate the wholesale market, presumably for call termination.

The main problem I have with the role of the EU is that they have reduced the game from a market-based approach to a lobbying-based approach. The mobile companies will now spend fortunes trying to get the legislation created in a way friendly to them. This nonsense has gone on from the beginnings of the creation of pan-European operators.

The difference in the USA is stark. After the creation of Verizon Wireless in 2000, local calling plans and tariffs immediately become national plans for the major networks. This is despite the fact that the big networks have patchy coverage across the States and has only been possible with individually negotiated roaming deals with regional players such as Alltel. Small local companies still exist today and offer local calling plans only with roaming options.

My own view is that it is the fault of the EU that cross-border products have not been developed as opposed to the operators.

I have been thinking of what I would do in Vodafone’s position. Undoubtedly, they could quite easily abolish roaming charges on-net. This would cost a large amount of revenue and would almost certainly need agreement with the Partners networks. The potential benefits of having larger call volumes and more customers are largely theoretical. However, with the introduction of the Passport scheme, Vodafone will have now been collating data for around 12 months of the price elasticity and reaction to marketing efforts. It will be extremely interesting to see the adjustments, if any, Vodafone make to the Passport scheme for the coming Summer European Holiday Season.

However, the fear of excessive regulation will also be there for Vodafone. If they are too aggressive, many of the other operators will complain and get the proposed legislation amended in their favour via the wholesale tariffs and open-access.

Vodafone is walking on a tightrope and its’ current position is extremely difficult especially when the stock market is putting pressure on it to prove the benefits of scale.

Flashback to April 2000, when VOD bought Mannesmann, there was a wave of complaints to Mario Monti, the EU commissioner at the time that VOD would be able to launch Pan-European services which the other operators would not be able to replicate. What is interesting is that these services, included not only the services that were available at time, such as voice roaming, but also included services that were not available at time such as location based services and corporate LAN access.

The EU also decided that VOD did have a dominant position in any of the services, but could enjoy a time-to-market advantage, because of complexities of negotiating deals for the other operators. In addition to the sale of Orange, Vodafone also undertook for a period of three years to offer the “same price & structure” to competitors if Vodafone lowered its’ Roaming charges.

In other words, Monti nullified any competitive advantage for Vodafone for three years in developing cross-border products & services. It is also interesting that the other operators complained that VOD would become dominant in buying handsets and the competitive advantage was discriminatory, which the commission disagreed with. The complete EU Vodafone/Mannesmann Ruling is here.

It is hardly surprising then that Vodafone did not launch the Passport product until May 2005. Although, the product targets only voice roaming charges and undoubtedly brings down the charges in a lot of markets, it can hardly be called a cross-border product, since the Pricing, Terms & Conditions vary by country.

Now, we have an ongoing investigation from the EU in roaming charges and the EU seems to now want to get rid of them:

• The new EU regulation should in any event address inter-operator tariffs (wholesale prices). The EU regulation would ensure that operators do not charge operators from other countries substantially more than the actual cost.

• To ensure that operator savings at the wholesale level are actually passed on to the consumer, the Commission sees also a need for regulation at the retail level.

• The new EU regulation could in particular eliminate all roaming charges for receiving a call when travelling abroad in the EU.

• In addition, for calls made while travelling abroad in the EU, the new EU regulation could introduce the “home pricing” principle. A mobile customer travelling abroad in the EU would always be charged only the prices that he is used to paying in his country of residence: he would either pay a local tariff when making a local call, regardless of where he is travelling in the EU (e.g. for calling a cab while travelling in Madrid); or a normal international tariff for calls made to EU destinations, regardless of where he is travelling in the EU (e.g. for calling the family back home while on holidays).

It does not take a genius to conclude that everyone from the largest to the smallest mobile operator will object to these principles. Basically, the EU wants to abolish roaming charges and regulate the wholesale market, presumably for call termination.

The main problem I have with the role of the EU is that they have reduced the game from a market-based approach to a lobbying-based approach. The mobile companies will now spend fortunes trying to get the legislation created in a way friendly to them. This nonsense has gone on from the beginnings of the creation of pan-European operators.

The difference in the USA is stark. After the creation of Verizon Wireless in 2000, local calling plans and tariffs immediately become national plans for the major networks. This is despite the fact that the big networks have patchy coverage across the States and has only been possible with individually negotiated roaming deals with regional players such as Alltel. Small local companies still exist today and offer local calling plans only with roaming options.

My own view is that it is the fault of the EU that cross-border products have not been developed as opposed to the operators.

I have been thinking of what I would do in Vodafone’s position. Undoubtedly, they could quite easily abolish roaming charges on-net. This would cost a large amount of revenue and would almost certainly need agreement with the Partners networks. The potential benefits of having larger call volumes and more customers are largely theoretical. However, with the introduction of the Passport scheme, Vodafone will have now been collating data for around 12 months of the price elasticity and reaction to marketing efforts. It will be extremely interesting to see the adjustments, if any, Vodafone make to the Passport scheme for the coming Summer European Holiday Season.

However, the fear of excessive regulation will also be there for Vodafone. If they are too aggressive, many of the other operators will complain and get the proposed legislation amended in their favour via the wholesale tariffs and open-access.

Vodafone is walking on a tightrope and its’ current position is extremely difficult especially when the stock market is putting pressure on it to prove the benefits of scale.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}